Goldman Sachs Raises Oil Price Forecasts Amid Strait of Hormuz Disruptions

Goldman Sachs Raises Oil Price Forecasts Amid Strait of Hormuz Disruptions

The alternative investment world is infamous for applying labels to itself, some of which are self-explanatory but many of which murky or just misleading. This series will demystify the jargon and explain the investment.

Part 1: Global Macro Strategies

Defining You know that the devaluation of the Chinese currency will have an immediate, and drastic, short-term effect on the markets – but you may not know the medium- to long-term effects. Another series of pundits espouses their tea-leaf reading expertise on the direction of crude oil. You know that these developments will bring opportunities and risks in the markets, and in any case will, no doubt, affect your own investments. But typically the only explanation you come across is how the yuan or oil will affect the stock markets that week. No bigger picture than that.

But this is not your fault. There is a knowledge gap between the popular press (or even your favorite web search engine) and the way to create wealth from political and economic drivers. The global macro manager is the investor that is rewarded for being able to connect dots in the fog of information (and misinformation).

To show that he or she gets the bigger picture, most Global Macro managers like to talk about their investment “themes.” Whether purely discretionary or aided by quant models nearly any macro manager worth their salt can recite his/her themes. The manager forms these investment themes based on his/her view of the medium- to longer-term economic and political drivers. These include supply and demand, global asset flows, and global geopolitical factors. But the ultimate goal isn’t to look like a wise sage, but to make your investors’ money by anticipating price movements. Most macro managers tend to capture the macroeconomic effects as they affect prices in the global equity, fixed income, and FX markets, and sometimes commodities markets as well.

A classic example of a macro trade might involve shorting the currency of a country that’s cutting its interest rates and buying that of a country raising rates, with the view that capital is attracted to the fixed income markets offering higher rates. But the seasoned macro trader also knows that much of this rides on expectations. Even if one country’s rates are higher, indications that monetary policy is easing (or should be eased) may disrupt the flows.

There’s also the political example. The South African parliament recently proposed a bill that would make it easier for citizens to sue or even expropriate holdings of foreign corporations. The bill was immediately viewed by the global community as decidedly anti-business, and the nation’s currency and stock market both dropped upon the news. Any price changes now will be reality being out of line with expectations, either positive or negative: If the bill trudges along as expected, these markets will likely continue a slow downtrend. However, if parliament lightens up the constraints a bit more than expected, both currency and stock market may rally; if a version toughens the penalties just the opposite.

Global macro managers can employ a variety of techniques and asset classes to capitalize on changing market environments. As BarclayHedge describes it: “Global macro strategies generally focus on financial instruments that are broad in scope and move based on systemic risk. Systemic risk or market risk is not security specific. In general, portfolio managers who trade within the context of global macro strategies focus on currency strategies, interest rates strategies, and stock index strategies”. In other words, the examples above, currencies may be the best way to play the divergent interest rate policies, rather than buying a corporate bond, and selling the overall South African market makes more sense than just shorting an individual stock.

However, while these strategies can offer high returns, the risks are high also. There are a myriad of developments that can take an investment theme off-track, including political and military events, natural disasters, and unanticipated and sudden news disclosures.

How Can Macro Help a Traditional Portfolio?

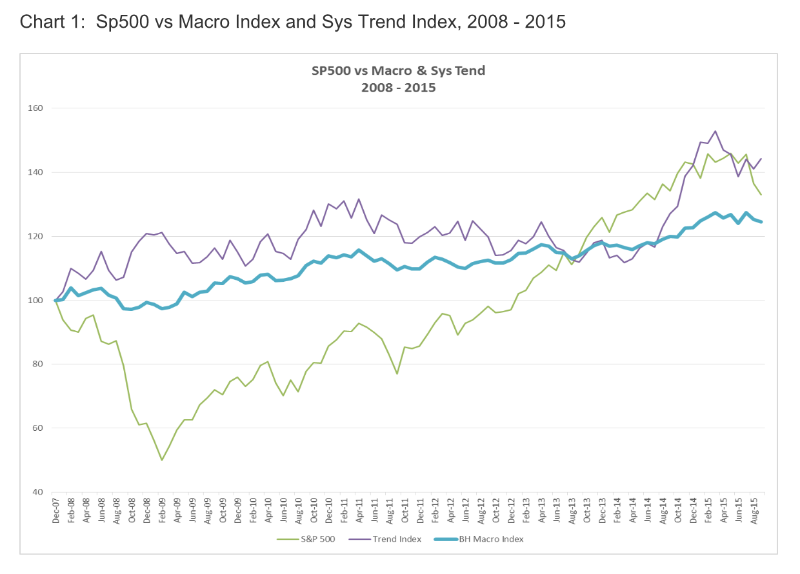

Chart 1 below includes an index of Global Macro programs (blue line) plotted against the S&P 500 index (green line) since January 2008. We have also included an index of systematic CTAs (purple line). The start date is a bit unfair, as 2008 was a disastrous year for global equities but quite good for macro (see Chart 2). But this is to prove a point.

Chart 1: Sp500 vs Macro Index and Sys Trend Index, 2008 - 2015

Past performance is not necessarily indicative of future results.

Chart 2: below shows average monthlies for how various indices performed just in 2008 alone.

This was not unusual. One of the best historical periods for global macro came during the burst of the Tech Bubble in March-April 2000. Almost all macro indices generated returns in excess of 15-20% over the subsequent 12 months – while global equities dropped -25.9%. Global macro funds also generated outperforming returns following the Asian crisis, when these funds were able to establish short positions across a range of Asian markets.

The basic idea behind investing in macro is to tap into a completely diversified set of returns. By covering multiple asset classes and the ability to go long or short in these asset classes, global macro brings investors a different source of returns than long equities or long bonds. They are therefore better equipped to perform in a range of economic environments. The challenges faced by traditional market sectors during crises tend to also present meaningful opportunities for macro strategies.

Different Flavors All macro programs are not created equal. The classic profile of the macro manager is the opinionated economist, trading according to his/her own discretion. Many still fit this description. With today’s tsunami of data and news zipping about the internet, however, the challenge is making sense of all this information (and misinformation). Even the most discretionary global macro manager relies on some form of quantitative tools or modelling to make sense of it all.

This is not to say that many global macro strategies do not incorporate some systematic or model-driven component. In fact today most do in some aspect of their strategy. Some macro strategies can almost completely model-driven, taking in economic and fundamental inputs. One sub-category of global macro that focuses on some form of relative value play – e.g. spreads, carry, or other convergence trades – tend to be model-driven.

Global Macro is not the only strategy that covers all the various asset classes on a global, macroeconomic level. It has a close cousin in Systematic Trend strategies (You can contrast Systematic Trend, the subject of our next installment, against the performance of global macro in the charts above.) In fact many systematic CTAs have taken to labelling their programs “systematic global macro,” which has resulted in some confusion in the marketplace. Most global macro managers, and their clients, insist that the trading of global markets is where the similarity ends. Macro strategies feed on economic and geopolitical information and tend to look for value, or relative value, typically with some discretionary input. In contrast, systematic trend strategies are driven by price alone, looking for momentum, not value. And the price data is almost always fed into an algorithm. The practical difference was once summed up by one investor:

The macro guy may be the first one at the party, but often the longest one to stay if it’s a dud and the first one to leave once it’s roaring; the systematic guy arrives when the party’s already roaring but is the last one to leave.

Global Macro In a Nutshell

Key Characteristics:

- A macroeconomic perspective on the markets

- A top-down investment style

- Global opportunity set

- Avoidance of low-liquidity markets

Key Performance Attributes:

- Times of economic disruption

- Rising or high volatility markets

About this series. Common to all good managers is the desire to push the limits of information and technology to gain an edge, regardless of label. But the labels do not necessarily help non-hedge fund pros to understand the categories and strategies--and figure out which ones belong in their portfolio. This is the first part of a series exploring the various categories of strategies we offer on the Hydra Platform, with the first installment focused on Global Macro strategies.

Next installment: Systematic Trend Strategies

About Kettera Strategies. We strongly believe in transparency and demystifying the hedge fund jargon so that investors can make informed choices. Our area of expertise is managed futures and we specialize in Global Macro strategies. However, our team and the 40+ managers on our Hydra platform offer an array of alternative investments. We also believe that knowledge is power. To that end, we’re creating a series of posts here that seek to objectively define hedge fund strategies, and use real time examples of how these hedge fund strategies work.