We've summarized AUDUSD FX option information in sequence of the vanilla options market in the sensitivity table which comprises of Black-Scholes implied volatilities for different maturities and moneyness levels.

And also see for the probabilities of different OTM and ITM strikes with their corresponding change in probability numbers as well as option greeks.

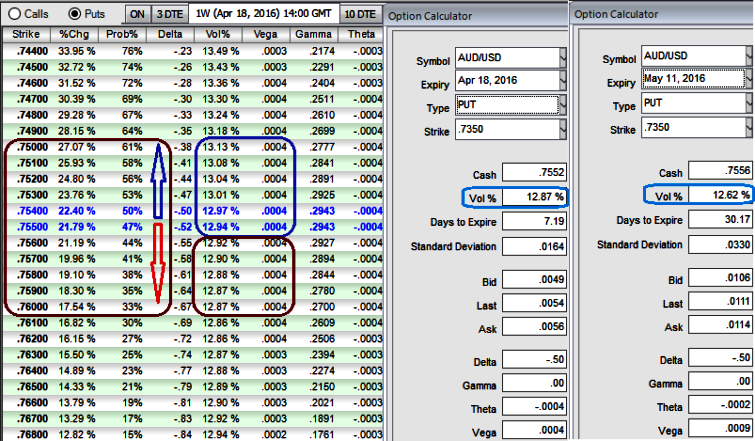

For an instance, from spot ref: 0.7552 if it drifts below 50 pips (i.e. 0.7502) and jumps above 50 pips (i.e. 0.7602), we see 27% change in option premiums in case of OTM strikes but 17.54% for the same 50 pips difference on the higher strikes (ITM).

Why is this difference even though 50 pips change in underlying price when all parameters remain same?

Now, let's have a glance on something called implied volatility, we consider IVs of 13.13% at 0.75 levels and 12.87% at 0.76 strike price.

The implied volatility as a function of moneyness for a fixed time to maturity is generally referred to as the smile. The volatility smile is the crucial object in pricing and risk management procedures since it is used to price vanilla, as well as exotic option books.

OTM strikes, rely solely on extrinsic value and have a low Delta, Theta, and Vega. But a move towards the OTM territory increases the ATM Vega, Gamma and Delta which boosts premiums.

The degree of moneyness of an option can be corresponded to the strike or any linear or non-linear transformation of the strike. (Forward-moneyness, spot-moneyness, delta).

For an instance, AUDUSD ATM vanilla option has IV at 12.87% for 1w maturities, 12.67% for 1m maturity, but on a strategy or of different strike it certainly varies.

When we choose a slightly out of the money strike put considering delta risk reversal computations, the relative volatility would also change. This is basically because market participants order flows does not expect the direction the strike price that is chosen.

That is because the market participants entering the FX OTC derivative market (heterogeneous) are confronted with the fact that the volatility smile is usually not directly observable in the market. This is in opposite to the equity market, where strike-price or strike-volatility pairs can be observed.

Over the longer-term, we expect AU growth to remain subpar and AUD to drift lower. There are a few key things to watch in 2016. Governor Stevens retires in Sept 2016 while a federal election must be held by Jan 2017. AU’s current account deficit is also worth tracking.