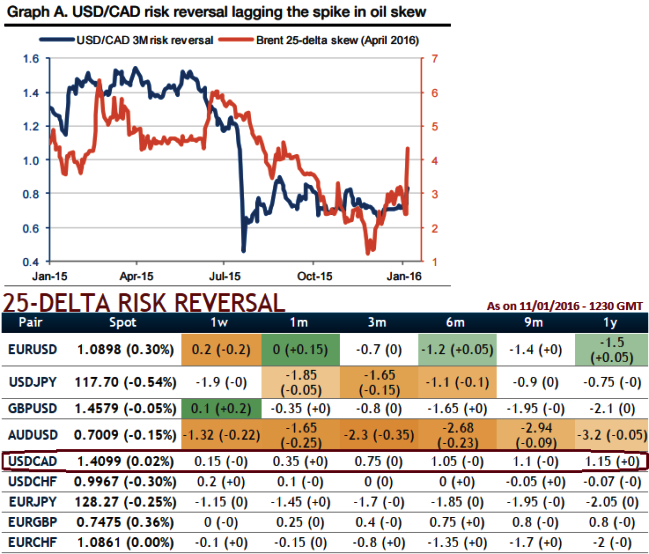

In response to the tumble in crude prices the options market shows an interesting disruption, while the correlation between oil and CAD is ultra strong.

The New Year series has been subdued for CAD: on the back foot largely as a result of tumbling crude oil prices.

The present-day situation has USDCAD trading to an 12-1/2 years high as crude oil prices forge a new cycle low below USD 30.50/brl mark.

This should maintain headwinds for the Canadian economy as we enter 2016, with GDP growth hampered by additional cuts to energy capital expenditures that, in turn, detract from business investment.

We could foresee no scenes of recovery in CAD unless this energy commodity bottoms up and shows signs of recovery as pr the forecasts.

As a result, the implied volatility of ATM options on both underlying assets rose in similar proportions, but OTM volatilities diverged substantially.

It turns out that OTM Brent puts became more expensive than OTM CAD puts. Considering an oil hedge in FX space is therefore a cheaper alternative.

Even if the FX skew lags the Brent skew, nonetheless it is bid for USD calls. Selling high strikes remains the best way to cheapen call options in USD/CAD.

We are revising our USDCAD profile higher in the short-term (1.45 for Q1 end) with the risk that we trade higher intra-quarter or CAD recovers sooner if oil manages to stage a rally.

Thus, we stress that the lack of a recovery in crude oil prices remains the most important risk to our CAD outlook. This would likely establish new stage for USDCAD bulls run in Q1 of 2016.

While OTC market sentiments indicates that upwards risks of underlying spot FX as risk reversal shows expensive hedging for upside risks.

Hence, we recommend it is better to cover all your last week shorts and go long in 1M ATM +0.51 delta call and 1M (1%) OTM 0.38 delta call and simultaneously short 1W 1 lot of ATM call (shorter expiry) in the ratio of 2:1.

The lower strike short calls because it finances the purchase of the greater number of long calls (ATM calls are overpriced, so we chose 1% OTM calls as well) and the position is entered for no cost or a net credit.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: Crude’s correlation with CAD makes OTM vols diverged – USD/CAD Call Ratio Back Spreads to hedge upside risks

Tuesday, January 12, 2016 7:49 AM UTC

Editor's Picks

- Market Data

Most Popular