Reducing Hedging Cost - Use short term upswings to stay short in long term:

Off-late, since we saw the Fed maintained unchanged rates, continuing on with its gradual tightening cycle in June.

We think current macro situations lead the fed to almost defer policy actions to June meeting, but manipulative statements on monetary policy outcome may keep USDJPY at stake.

On the other hand, we can very much empathize with this Yen against dollar to gain slightly at least in short run (let's say next 2 months or so) with an anticipation of Fed may continue to hold on its rate stance until Q2'16 considering global economic slowdown.

Elsewhere, let's have a glance on OTC market arrangements for hedging the uncertainty in this pair:

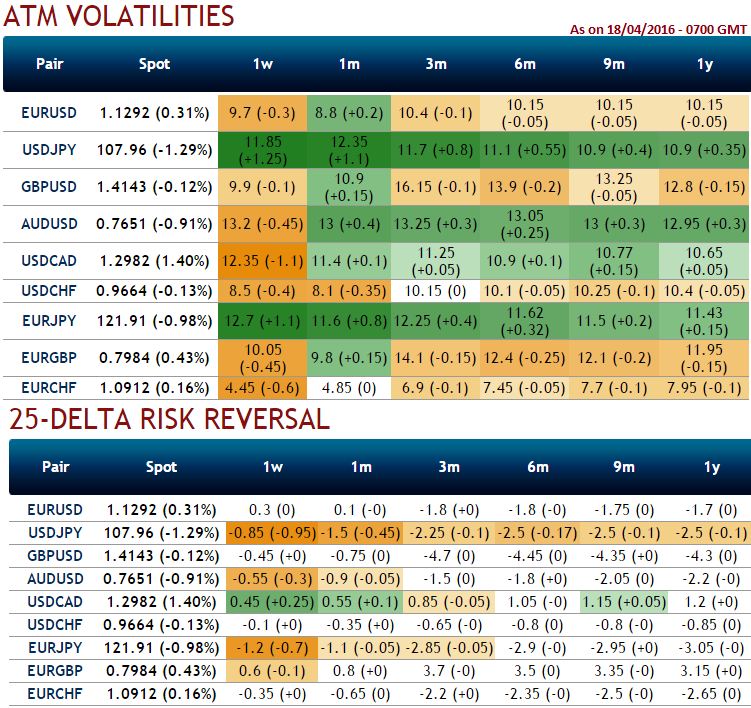

OTC risk reversal for USDJPY in long term is in the one of the top three pairs that means hedging activities are mounting up ahead of monetary policy seasons across the different central banks.

IVs for next 1 months contracts reasonably higher at around 12.35% but the same ATM contacts of 1-3 expiries have gradually reduced implied volatilities that is unlikely evidence any change in its rate policy that may prop up dollar's strength in future (see and compare current 1w & 1m contracts with 3m-1Y tenors).

Most importantly, delta risk reversal for the pair is still the highest negative values among entire G10 currency space for all expiries, so we believe any short upswings are the best advantage for bears and may be utilized for shorts in hedging strategies so as to reduce the hedging costs. (Compare delta risk reversal with last week).

The pair is likely to perceive implied volatility close to 11.85% of 1W ATM contracts that would likely decrease to 11.5% with increase in negative risk reversals, thus we recommend deploying short put ladder spreads that contains proportionately less number of shorts and more longs which would take care of potential slumps on this pair and significantly higher volatility times.

This would mean that market sentiments for this pair have been bearish for this pair. As a result, we reckon that for next 2 months time Yen may pretty much gain out of lots of manipulations and ambiguities are surrounding around dollar.

So, short ITM put with shorter expiry since implied volatility is inching higher when risk reversals are lesser comparatively to 1M expiries which is favourable for option writers in next 1 week or so, thus the strategy would be, go long in 2 lots of ATM and OTM put with longer expiry (per say 2M expiries) and simultaneously short 1W ITM puts with positive theta values. If you find it to be effective and accurate then, one can even think rising the weights in this strategy to 3:2.