JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026

JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026  DOJ Grand Jury Investigates UAW President Shawn Fain Ahead of Union Election

DOJ Grand Jury Investigates UAW President Shawn Fain Ahead of Union Election  Goldman Sachs Flags 3 Key Risks Ahead of Europe’s Earnings Season

Goldman Sachs Flags 3 Key Risks Ahead of Europe’s Earnings Season  Trinidad Businessman Dominic Hadeed Appeals Detention Over Alleged Assassination Plot

Trinidad Businessman Dominic Hadeed Appeals Detention Over Alleged Assassination Plot  Goldman Sachs Raises USD/JPY Forecast, Sees Yen Weakness Persist Through 2027

Goldman Sachs Raises USD/JPY Forecast, Sees Yen Weakness Persist Through 2027  US Inflation Expected to Ease in June, but Fed Rate Hike Risks Persist Amid Middle East Tensions

US Inflation Expected to Ease in June, but Fed Rate Hike Risks Persist Amid Middle East Tensions  DOJ Seeks Dismissal of Gautam Adani Bribery Case, Citing Foreign Scope

DOJ Seeks Dismissal of Gautam Adani Bribery Case, Citing Foreign Scope  Paramount-Warner Bros. Discovery Merger Faces Lawsuit From 12 States

Paramount-Warner Bros. Discovery Merger Faces Lawsuit From 12 States  Texas Man Charged After Fatal Tesla Full Self-Driving Crash in Katy

Texas Man Charged After Fatal Tesla Full Self-Driving Crash in Katy

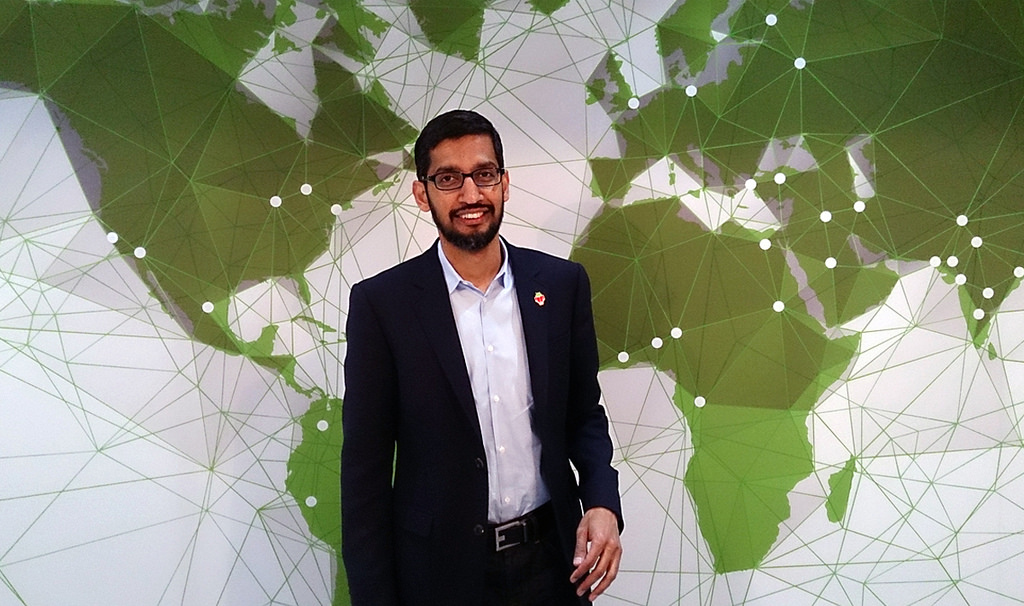

Google CEO Sundar Pichai has earned an eye-popping pay rise. He was awarded US$199m in shares, according to a recent filing with the US Securities and Exchange Commission. It makes him the highest-paid chief executive in the US and though he sits at the top of the pile, news of his or any CEO’s big pay rise will come as little to surprise to many.

CEO compensation has grown at an alarming rate over the last three decades. In 1980 most CEOs at major British companies earned around 15 times the average salary. By 1998 the ratio of CEO to average worker pay was 47:1. In 2014 it had ballooned to roughly 183:1.

In the US, the ratio is even higher. According to the AFL-CIO, a federation of labour organisations, the salary of a typical S&P 500 company CEO in 2014 was 373 times the salary of an average rank-and-file worker – that’s US$13.5m compared to US$36,000.

How did we get here?

Some commentators aim to justify high pay on the grounds of company performance and that the efforts of these highly-skilled individuals is pivotal for a company’s success. These claims, however, are not supported by the research. CEO skill has been found to have more influence over captive corporate boards, not-so-independent remuneration committees and beholden compensation consultants in the ratcheting up of CEO pay. And the runaway train that is excessive compensation, shows no sign of slowing down.

CEO pay began to increase following calls for pay to be more closely pegged to a company’s performance. But if the intent was for growth in pay to keep pace with growth in firm performance, this hasn’t been achieved. The reality is that growth in CEO pay has continuously outpaced company performance – as measured by revenues and profits – even outpacing the FTSE 100 index itself.

These days the typical CEO’s pay packet comprises a salary, an annual bonus, and an equity-based component – usually in the form of long-term incentive plans and other short-term awards in the shape of company stocks and shares, as Pichai received. In this regard, the 1980s were a watershed period, largely due to the introduction of share-based schemes, which are partly responsible for the explosion in CEO pay levels. The same has not happened for average wages, yet the benefits of increasing them extend beyond the employee, and have the potential to benefit businesses, as well as individuals.

Pay ratios are the way forward

Making it mandatory for companies to publish their pay ratios is one way to curb excessive growth of executive pay and income inequality. This is a solution Jeremy Corbyn, leader of the Labour Party in the UK, put forward in a recent speech and – perhaps more powerfully than a suggestion made by a left-leaning leader of an opposition party – is being introduced in the US.

The Securities and Exchange Commission, the main Wall Street regulator, voted in favour of the rule last year and it will become mandatory for most public companies to regularly reveal the ratio of CEO pay to that of employees as of 2017.

Although UK companies are currently required to disclose CEO compensation as it compares with their employees, they are not required to disclose long-term pay incentives, such as shares, which are a large component of current executive pay packets. And they are only required to compare the amount of CEO compensation with the pay of a select group of employees, not that of every worker.

The publication of pay ratios will likely help to reduce pay inequality as a result of the outrage that ratios would produce. In their book on executive pay, Harvard and Berkeley academics Lucien Bechuk and Jesse Fried, outline some of the problems with how pay is determined. They emphasise the importance of “outrage” when it comes to reversing the trend of CEOs setting their own, inflated compensation packages.

Flaws in the way that companies are governed mean that CEOs are largely constrained by the reaction of outsiders when it comes to setting their compensation arrangements. This reaction could range from mere criticism of pay arrangements to fully-fledged outrage in the vein of the Occupy Wall Street movement. Only when outrage is high enough does it function as an effective deterrent.

A mandatory rule requiring the publication of top-to-bottom pay ratios could therefore have two potential effects. It may force corporate boards to rethink excessive CEO pay and would hopefully force an increase in the pay offered to lower-level employees as well.

Tobore Okah-Avae does not work for, consult, own shares in or receive funding from any company or organization that would benefit from this article, and has disclosed no relevant affiliations beyond the academic appointment above.

Tobore Okah-Avae does not work for, consult, own shares in or receive funding from any company or organization that would benefit from this article, and has disclosed no relevant affiliations beyond the academic appointment above.

Tobore Okah-Avae, PhD Candidate in Corporate Law, Lancaster University

This article was originally published on The Conversation. Read the original article.