China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns

Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns  Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum

Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

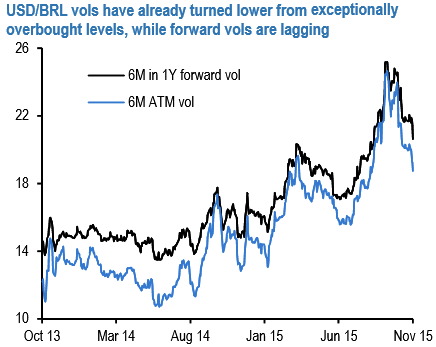

Short 6M in 1Y time FVAs in USD/BRL: Since Funding valuation adjustment is essentially the funding cost/benefit resulting from borrowing or lending the shortfall/excess of cash arising from day-to-day derivatives business operations (for an instance, posted and received collateral).

These collaterals are radically contrarian position that should sustain in reasonably well even if we do get the 6% drop in the real that it is pencilled in for H1.

ATM vols in USD/BRL have already turned lower from remarkably overbought levels aided by soft realized performance in recent weeks (3-4 pts. under) yet forward vols are lagging and are priced 2-2.5 vols above.

We would not like to disregard the probabilities of vol bouncing back again in the short run, and BRL spot FX certainly can swing wildly in a way that would make selling realized vol (gamma) a distinctly uncomfortable stance to take.

But think that 20-handle forward vols will have a hard time realizing by the end of the year when greater clarity would have emerged on Brazilian politics and EM overall would have settled down after initial Fed-related tremors.

Hence our decision to take gamma out of the equation via an FVA short that benefits from implied vols falling short of what forwards price in by end-2016.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: FVAs in USD/BRL as vols turning lower in H1 2016

Tuesday, January 19, 2016 2:25 PM UTC

Editor's Picks

- Market Data

Most Popular