U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Macro outlook: In japan, Business sentiment improved from the end of last year, but remains cautious.

The PMI rose in March as services strengthened and manufacturing declined.

Wage inflation remained anemic in February.

Inflation expectations have been flat since the BoJ introduced its inflation overshoot commitment.

JPY has broadly appreciated against the major currencies.

As a result, JPY has reached the highest levels since last November both against NZD (refer above technical chart) and also on trade-weighted terms.

In NZ, Strong inbound migration to nudge Kiwi retail card sales higher

In the NZIER’s quarterly survey of business opinions, stronger pricing-related measures somewhat offset a general softening in confidence and expected activity indicators in 1Q.

NZIER reports confidence pulling back in the retail and manufacturing sectors in particular, while businesses in Auckland appear to be feeling the localized spillovers from prudential tightening that have slowed the housing market and taken some heat out of the consumer.

In the last six months, the confidence index in Auckland has dropped from 31 to 6. The headline confidence index fell from 28 in 4Q to 17 (net % positive), and by a little less in seasonally adjusted terms.

Indices of trading activity last quarter and in the quarter ahead faded 5-6pts, but both were steady in sa terms. These measures appear to have lost some of their predictive power over GDP in recent years and have consistently overshot actual performance.

China reported trade surplus a USD 23.9 billion in March of 2017, compared to a USD 25.2 billion surplus a year earlier and above market expectations of a USD 10 billion surplus. Exports surged by 16.4 pct YoY, following a 1.3 pct drop in February while markets anticipated a 3.2 pct growth. Imports rose 20.3 pct, after jumping 38.1 pct in the prior month and above consensus of an 18 pct rise.

China has been the major trade partner of New Zealand. As the kiwis' trade exposure towards China is considerable, we cannot afford to disregard ongoing upswings in underlying spot FX.

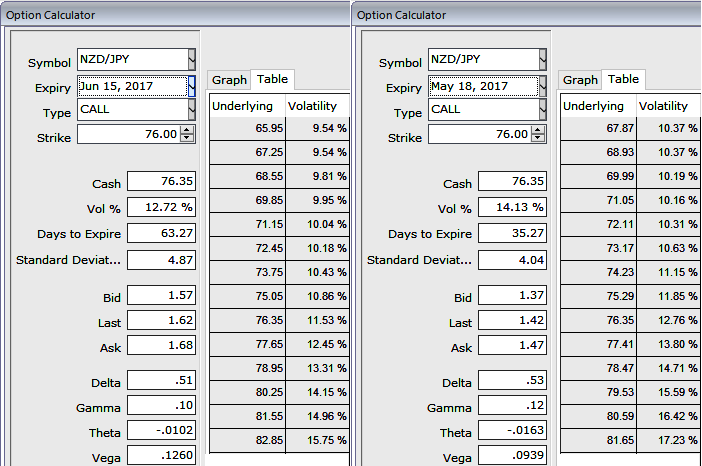

OTC Outlook and Options Strategy:

ATM IVs of this pair is trading at 14.13% and 12.72% for 1 and 2m tenors respectively. While 1m ATM puts are trading just at 8.97% more than NPV.

Compared to short selling of the underlying spot FX, it appears to be more appropriate to bet against underlying spot by adding longs in ATM put options as the investor does not have to borrow the underlying outrights to short.

Moreover, the risk is capped to the extent of initial premium paid, as opposed to unlimited risk when short selling the underlying outright.

However, put options have a limited lifespan. If the underlying FX price does not move below the strike price before the option expiration date, the put option will expire worthlessly.

Sell NZDJPY 1Y 25D RR and buy a 2m 75 NZDJPY OTM put, sell a 1m in premium-rebate notionals.