RBI Holds Interest Rates at 5.25%, Cuts India Growth Forecast Amid Rising Global Risks

RBI Holds Interest Rates at 5.25%, Cuts India Growth Forecast Amid Rising Global Risks  Fed’s Anna Paulson Signals Rates Could Stay Higher Longer Amid Inflation Risks

Fed’s Anna Paulson Signals Rates Could Stay Higher Longer Amid Inflation Risks  US Weighs Using Frozen Iranian Assets to Rebuild Gulf Infrastructure After Regional Attacks

US Weighs Using Frozen Iranian Assets to Rebuild Gulf Infrastructure After Regional Attacks  US Dollar Dips as Middle East Tensions Ease; Markets Await Key US Inflation Data

US Dollar Dips as Middle East Tensions Ease; Markets Await Key US Inflation Data  Asian Currencies Stabilize as Strong U.S. Jobs Data Boosts Dollar and Fed Rate Hike Expectations

Asian Currencies Stabilize as Strong U.S. Jobs Data Boosts Dollar and Fed Rate Hike Expectations  Indonesia Passes New Central Bank Law, Raising Investor Concerns Over Policy Independence

Indonesia Passes New Central Bank Law, Raising Investor Concerns Over Policy Independence  Oil Prices Rise as Iran-Israel Tensions Ease Following Trump-Led Ceasefire Push

Oil Prices Rise as Iran-Israel Tensions Ease Following Trump-Led Ceasefire Push  Uruguay Central Bank Holds Interest Rate at 5.75% Amid Inflation and Oil Price Concerns

Uruguay Central Bank Holds Interest Rate at 5.75% Amid Inflation and Oil Price Concerns  Australian Consumer Sentiment Drops in June as Financial Concerns Weigh on Households

Australian Consumer Sentiment Drops in June as Financial Concerns Weigh on Households  China Trade Surplus Surges in May 2026 as Exports and AI-Driven Imports Accelerate

China Trade Surplus Surges in May 2026 as Exports and AI-Driven Imports Accelerate  ECB Signals Possible Rate Hike as Middle East Tensions Push Euro Zone Inflation Higher

ECB Signals Possible Rate Hike as Middle East Tensions Push Euro Zone Inflation Higher  Gold Prices Hit 11-Week Low as Strong U.S. Jobs Data Dampens Rate Cut Hopes

Gold Prices Hit 11-Week Low as Strong U.S. Jobs Data Dampens Rate Cut Hopes  Dollar Near Two-Month High as Strong U.S. Jobs Data Boosts Fed Rate Hike Expectations

Dollar Near Two-Month High as Strong U.S. Jobs Data Boosts Fed Rate Hike Expectations  Jerome Powell Warns Against Politicizing the Federal Reserve, Defends Democratic Institutions

Jerome Powell Warns Against Politicizing the Federal Reserve, Defends Democratic Institutions

The Bank of England has increased its benchmark interest rate to 4.5% – the seventh rise since May 2022, when the base rate was just 1%. It is now at the highest level since 2008.

The European Central Bank (ECB) also increased its benchmark rate to 3.25% at its latest meeting in early May and is now nearing a high not seen since 2001. A few days before, the US Federal Reserve increased its rate from 5% to 5.25%, the highest level since mid-2007 and its 10th consecutive increase in just over a year.

Both central banks are nearing the end of their rate-tightening cycles as price pressures fall from a peak and the world anticipates a looming credit crisis.

But plans could change depending on how the economy fares. And whether we can expect the same from the Bank of England could depend more on the fragility of the banking system than the need to continue to tame inflation.

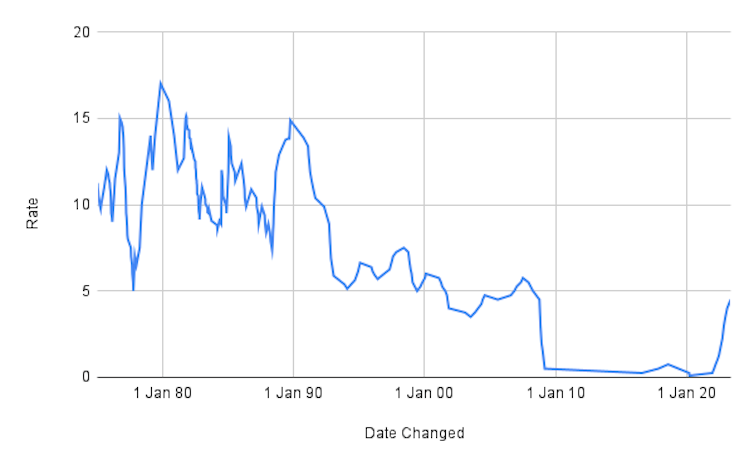

The UK’s new 4.5% base rate may seem high, but it’s actually quite low compared to the 1980s and 1990s. During these decades, the rate peaked at 16% and 13.88% respectively, but was always higher than 5%. These high rates reflected a similar battle with high inflation by the bank as it is dealing with today.

Low base rate today versus 1980s and 1990s:

So why are today’s interest rates at such (relatively) low levels? This is because of the toolkit central banks use to tackle rising prices, in particular base rate adjustments.

Like the Fed and the ECB, the Bank of England is trying to hit an inflation target of 2%. The latest official UK data shows inflation is at 10.1%, considerably above this target.

Inflation is measured by tracking the yearly change in the prices of a “basket” of goods and services that includes items like food, petrol and leisure activities. Surging energy prices following Russia’s invasion of Ukraine last February caused inflation to spike but have now been priced in to the annual measure.

Now food prices are keeping it elevated with a 19% rise over the year to March – the fastest increase in over 45 years.

Interest rate changes are a blunt tool to control such price rises without severely denting economic activity. A good example of this is when the US suffered painful inflation during the 1970s.

It took a crackdown by cigar-chomping Fed chairman Paul Volcker to break the cycle of rising prices and wages. He slammed the brakes on the economy by raising interest rates to 20%. Volcker’s actions worked: inflation retreated from 14.8% in 1980 to just over 3% by 1983. But 4 million people lost their jobs in recessions in the early 1980s.

Paul Volcker smokes a cigar while testifying before the House Banking Committee in 1986 during his time as US Federal Reserve Chair. mark reinstein/Shutterstock

Three effects of central bank decisions

Even without such drastic rate changes, such monetary policy decisions affect the wider economy and inflation in three main ways. Economists call these transmission channels.

The most obvious of the three is the interest rate channel because the changes in a central bank’s rates affect other interest rates such as mortgages. Higher rates will translate into higher repayments and less cash to spend on other things. Less spending means that businesses will be reluctant to increase their prices, which should lower inflation.

Interest rates also affect the real economy and inflation through the credit channel. It covers lending to both businesses and people. This can be seen through the availability of bank loans, as well as business balance sheets and risk taking.

When interest rates rise, the risk that some borrowers cannot safely repay their debts may increase so much that a bank will not lend any more money to them. These borrowers are then forced to stop spending or investing. This helps reduce inflation because less demand for products or services encourages companies to cut prices.

Changes in interest rates also affect firms’ balance sheets. An increase in interest rates lowers the value of things a company owns such as a building. In a higher rate environment, the property will be worth less, which matters if a business wants to use it as collateral on a loan for further investment in the business.

The effects of rate decisions on risk taking is thought to operate in two ways. First, low interest rates boost asset (and collateral) values. This, along with the belief that an increase in asset values will last for a long time, leads both borrowers and banks to accept higher risks. Second, low interest rates make riskier assets more attractive because investors must search for higher yields to make returns.

So, when interest rates are low, banks relax their lending rules, which can lead to an excessive increase in loan supply. This pumps more money into the financial system. Rate increases have the opposite effect.

Banking crisis fears

These effects can be seen recently via banking failures, most notably Silicon Valley Bank and Credit Suisse. While they happened for different reasons, both collapses exposed regulatory failures and poor risk management. Both were also triggered by tightening credit conditions, and by the increase in interest rates related to central bank rate hikes.

Such financial fragility should be expected in any parts of the banking system that are badly managed, poorly regulated and more exposed to tight credit conditions. This means another banking crisis could happen, especially if central banks continue to tighten monetary policy.

The Bank of England takes all of this into account when deciding on the next move for interest rates. And so, if it has stopped raising rates for now, it’s not because inflation has been tamed but because the risk to the banking industry is too great at the moment.

The authors do not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and have disclosed no relevant affiliations beyond their academic appointment.

The authors do not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and have disclosed no relevant affiliations beyond their academic appointment.