Goldman Sachs, ANZ Cut Oil Forecasts Amid U.S.-Iran Ceasefire Hopes

Goldman Sachs, ANZ Cut Oil Forecasts Amid U.S.-Iran Ceasefire Hopes  U.S. Strikes on Iran Draw War Crimes Warnings from International Law Scholars

U.S. Strikes on Iran Draw War Crimes Warnings from International Law Scholars  Goldman Sachs Cuts 2026 Copper Price Forecast Amid Global Growth Concerns

Goldman Sachs Cuts 2026 Copper Price Forecast Amid Global Growth Concerns  Private Credit Under Pressure: Is a Slow-Motion Crisis Unfolding?

Private Credit Under Pressure: Is a Slow-Motion Crisis Unfolding?  Morgan Stanley: Fed Rate Cuts Still on Track Despite Oil-Driven Inflation

Morgan Stanley: Fed Rate Cuts Still on Track Despite Oil-Driven Inflation  How will the Iran war change the Middle East? We asked 5 experts

How will the Iran war change the Middle East? We asked 5 experts  Gold Loses Shine as Crude Oil Surges: Safe-Haven Metal Retreats Toward USD 4,500 Support

Gold Loses Shine as Crude Oil Surges: Safe-Haven Metal Retreats Toward USD 4,500 Support

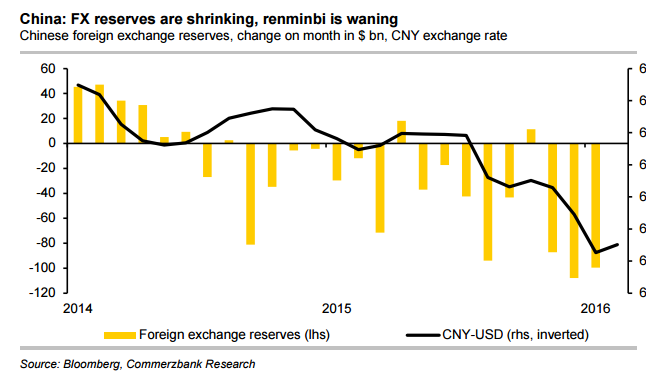

Just about six months ago, China held as much as $4 trillion in foreign exchange reserves. The country's foreign exchange reserves are shrinking steadily on money outflows and as Beijing moves to shore up its currency. Reserves have shrunk by nearly a fifth since the summer of 2014. In January alone, reserves fell by some $100bn, having declined by 19% since their peak in August 2014.

Still at $3.231 trillion the PBoC's foreign exchange reserves are extremely healthy - better than any other central bank. But the situation cannot be sustained for long and at some point, even the large PBoC reserve portfolio will disappear, if nothing changes. The PBoC then, will no longer be able to support the currency via forex sales, and there is a possibility that the renminbi would plummet.

The reason behind the depletion of reverses is China's export earnings are not sufficient at present to finance the capital exodus. Chinese trade data released earlier this week showed that export growth was -11.2% y/y, the lowest reading since March 2015. The disappointing export figures served as a stark reminder of the continued weakness in external demand. The gap is being bridged by the Chinese central bank selling its forex reserves.

The PBoC has three options: sudden, massive devaluation; gradual devaluation or clear restrictions on cross-border capital flows. Chinese authorities are adopting a mixed strategy which includes moderate depreciation as well as an imperceptible reigning-in of capital outflows and this muddling through will likely continue for now.

"In our view, a policy of muddling through could well prove successful. If the strategy doesn't work, unpleasant decisions would have to be taken. But rather than risk a collapse of the exchange rate and a sharp recession, the government would prefer to place stronger, more visible restrictions on capital movements." said Commerzbank in a report.

The yuan edged down against the dollar on Friday after the central bank set the midpoint rate at 6.5186 per dollar, only 0.05 percent weaker than the previous fix of 6.5152. The spot market opened at 6.5190 per dollar and was trading at 6.5203 at midday, while the offshore yuan was trading 0.11 percent weaker than the onshore spot at 6.5275 per dollar. On Thursday, the PBoC stated that it would conduct open market operations every working day, providing flexibility in its efforts to aid the banking system without needing to resort to broad interest rate cuts and thus putting downward pressure on the yuan.

"We expect renminbi to devalue further but without plummeting. We consider it likely that USD-CNY will gradually rise until just short of 7.00 rather than reaching extreme levels far beyond this level." adds Commerzbank.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

China’s exchange rate policy likely to keep markets on edge

Friday, February 19, 2016 11:02 AM UTC

Editor's Picks

- Market Data

Most Popular