Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Recently there has been some concern over Euro/Dollar trade, while some analysts are pointing out that Euro might take further dip, especially with further easing from European Central Bank (ECB) as early as next hour, whereas others are pointing to Euro might be too over-shorted. Goldman Sachs is calling for rates below parity and as low as 0.8 for the pair by next year, whereas Wells Fargo is calling for Euro as high as 1.2 against Dollar.

We, thought it would be good idea to evaluate the confusion, from fundamental point of view.

In our pursue for fundamental evaluation, we look at the following -

- Big Mac index

- Purchasing power parity

- Long rates

- Short rates

- Ultra-short rates

- Policy divergence

- Current account

In our previous fundamental evaluation articles we have already reviewed Euro and Big Mac, policy divergence and in this one we focus on short rates.

Why short rates?

Short term interest rates can determine investment flows especially in fixed income. If Euro interest rate is lower and Dollar rates are higher, it makes sense to borrow in Euro and invest in Dollar. Assuming exchange rate remains steady, one can make higher interest rates. Since exchange rates hardly stays the same, more flows to Dollar would move the Dollar higher against Euro.

Short rates are more vital than ever in today's financial world, where central banks globally has introduced monetary stimulus worth $25 trillion, among which FED itself introduced close to $4 trillion. Low yield environment, makes the hunger for yield more than ever.

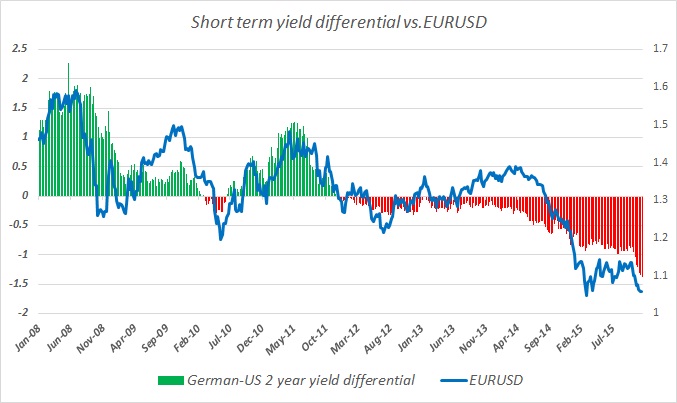

Short rates and EUR/USD -

As shown figure, Euro/USD since the crisis is showing high level of correlation with differential in short term interest rates. Euro usually drops, when short term (2 year used for calculations) interest rate differentials are in decline or in favor of Dollar.

In January 2008, Yield differential between 2 year German bond (German Schatz is used as it is widely accepted Euro zone benchmark risk-free bond) and 2 year US treasury was at 1.13% and Euro was trading at 1.46 against Dollar. That differential as of this week standing at -1.38% and Euro is trading at 1.055 against Dollar.

Yesterday, While German 2 year yield dropped to lowest on record at -0.44%, Us 2 year treasury hit new recent high at 0.94%

Evidence suggest, Euro is likely to continue drop further against Dollar, if yield divergence continues.