World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

The unemployment rate is sufficient to demonstrate the calculated case to long NOK. The jobless data is exactly the same as it was at 2.7% when Brent was at the peak $115 last summer.

So one could be thinking by now what has that factor got to do with the new oil market realities, even if a lagged rise in unemployment is to be expected.

This is not to deny that a halving of the oil price will have a material effect on the economy, of course it will, it's just that the magnitude of the downturn is proving less intense than many, including the Norges Bank, believed (1Q GDP growth was reported this week at 2.0% saar).

The currency shake-off is likely event if an economy is associated with global oil trade terms. The psychological oil-slick means that NOK is the cheapest G10 currency whereas GBP is virtually the most expensive, in other words these are good entry levels for a tactical trade that exploits a potential rebound in oil prices over July and August.

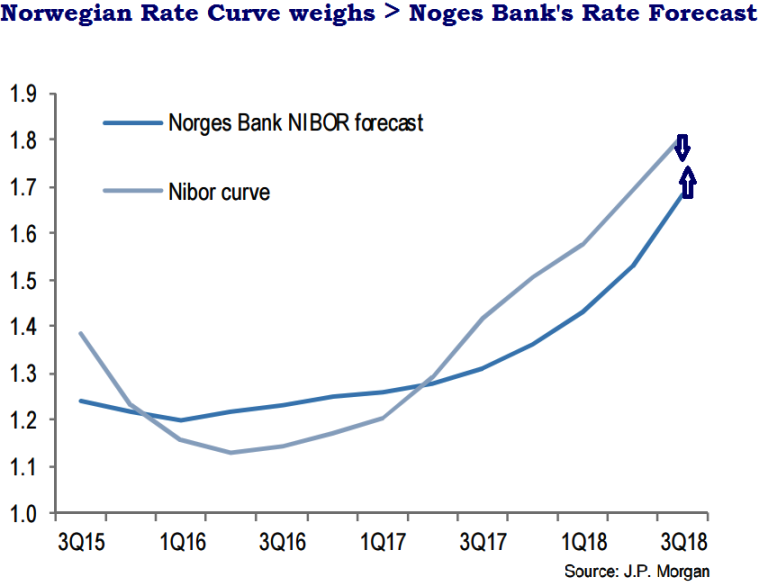

The Norwegian rate curve prices more cuts through 201 than the Norges bank's path which limits downside for NOK.

As shown in the diagram, Norges Bank rate cut on June 18th may depress NOK since the NOK rate curve is already priced in for marginally more easing than the central bank's projections.

Ahead of the rate decision, the preliminary energy sector capex survey for 2016 is scheduled on June 12.

This will have a potential bearing on the Norges Bank's longer-dated rate guidance to the extent that it shows the slide in capex continuing into 2016 or starting to wind down.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Any hike in oil prices impacts adversely on sterling; monetary policy on NOK

Wednesday, June 3, 2015 12:33 PM UTC

Editor's Picks

- Market Data

Most Popular