Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions  SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation

SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation  How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform

How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

ECB President Mario Draghi will also be speaking in Jackson Hole – and before that in Lindau, Germany. The FX market will mainly want him to say whether the euro strength seen over the past months is beginning to get too much for him. That is what the European central bankers had expressed in the wording of their meeting minutes. If Draghi does not say anything on the matter this could be seen as an attempt to back paddle, strengthening the euro further. That would not be in the interest of the ECB head his speeches.

Nevertheless, his speeches are always partly contextual. In particular in Jackson Hole – usually, a good place for fundamental strategic comments – an obvious verbal intervention against euro strength would not be appropriate, as representatives of all central banks will be present who have promised each other not to manipulate exchange rates – not even verbally.

We already pronounced that the view of front-end vols will stay well-supported as August, in general, tends to be a seasonally strong month for volatility, and the investors seem inadequately invested in the bullish Euro trend judging from the breadth and intensity of spot rallies and counter-conventional spot-vol correlations so far, so directional option demand is likely to remain robust, as per the JP Morgan’s stances.

The Kansas Fed’s August 24th - 26th Jackson Hole conference where Mario Draghi is slated to speak two weeks before the September 7th ECB meeting will provide a natural magnet for such option flows, as investors sniff for hints around the ECB’s tapering intentions. 1-month option expiries rolled over the Jackson Hole dates this week, and 1M ATMs in Euro-and Euro-crosses have jumped to reflect the elevated day-weight (21% O/N vol) being assigned to the event.

Despite the repricing in option prices over the past few weeks, we see a couple of option opportunities that still offer value around the bullish Euro theme:

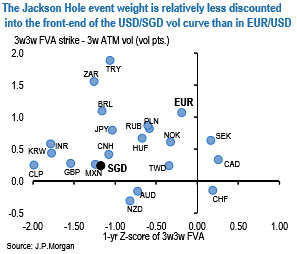

Judging whether the Jackson Hole event weight is excessive for a single currency is tricky, but it is easier to identify vol curves where this risk premium is underpriced relative to EURUSD. Using the slope of the 3-wk/6-wk ATM (pre-Jackson Hole vs. post ECB/Fed) curve as a proxy for the event risk premium, USDSGD stands out as an underpriced candidate that has tracked EURUSD with 60% correlation in spot returns over the past month –not surprising given the ~13% JPM-estimated weight of EUR in the SGD basket - and where forward vol is both low on levels and almost flat to spot ATM (refer above chart).

As a bearish dollar play with a positive carry lean, short 3-wk vs. long 6-wk 1.3450 strike USD put/SGD call one-touch option calendars are well priced ~20% (1.3610 spot) and accrue smalls positively (~1.3X) in premium on a static basis, which can be monetized if SGD remains sandwiched between offsets of broad dollar weakness and richness within the SGD NEER band (+88bp at the time of writing) over the next month until given a move on by Dr. Draghi.