FxWirePro: NZD/USD retreats as Middle East instability weighs

FxWirePro: NZD/USD retreats as Middle East instability weighs  FxWirePro: GBP/USD eases as dollar firms ahead of U.S. June non-farm payrolls report

FxWirePro: GBP/USD eases as dollar firms ahead of U.S. June non-farm payrolls report  FxWirePro: EUR/AUD slips after surprise U.S. employment data

FxWirePro: EUR/AUD slips after surprise U.S. employment data  FxWirePro: GBP/AUD under pressure after disappointing U.S. employment data

FxWirePro: GBP/AUD under pressure after disappointing U.S. employment data  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  FxWirePro: GBP/USD rises as weak U.S. jobs data pressures dollar

FxWirePro: GBP/USD rises as weak U.S. jobs data pressures dollar  NZDJPY Bears Lie in Wait: Sell Rallies at 93 for 90 Target with 94 Stop

NZDJPY Bears Lie in Wait: Sell Rallies at 93 for 90 Target with 94 Stop  FxWirePro: GBP/AUD eases slightly, focus on near-term support

FxWirePro: GBP/AUD eases slightly, focus on near-term support  FxWirePro: EUR/ AUD neutral in the near term, scope further downside

FxWirePro: EUR/ AUD neutral in the near term, scope further downside  FxWirePro : USD/CAD falls as strong Canadian jobs data lifts loonie

FxWirePro : USD/CAD falls as strong Canadian jobs data lifts loonie  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  DAX & CAC40 Score Perfect 100: Extremely Bullish With Major Levels to Watch as FTSE100 Hits 80

DAX & CAC40 Score Perfect 100: Extremely Bullish With Major Levels to Watch as FTSE100 Hits 80  FxWirePro- Woodies pivot (Major)

FxWirePro- Woodies pivot (Major)  FxWirePro: USD/CNY slips as strong China exports data Lift yuan

FxWirePro: USD/CNY slips as strong China exports data Lift yuan  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  Major Pair Currency Score: NZD/USD and AUD/USD Lead Forex Rally with Perfect 100 Scores

Major Pair Currency Score: NZD/USD and AUD/USD Lead Forex Rally with Perfect 100 Scores

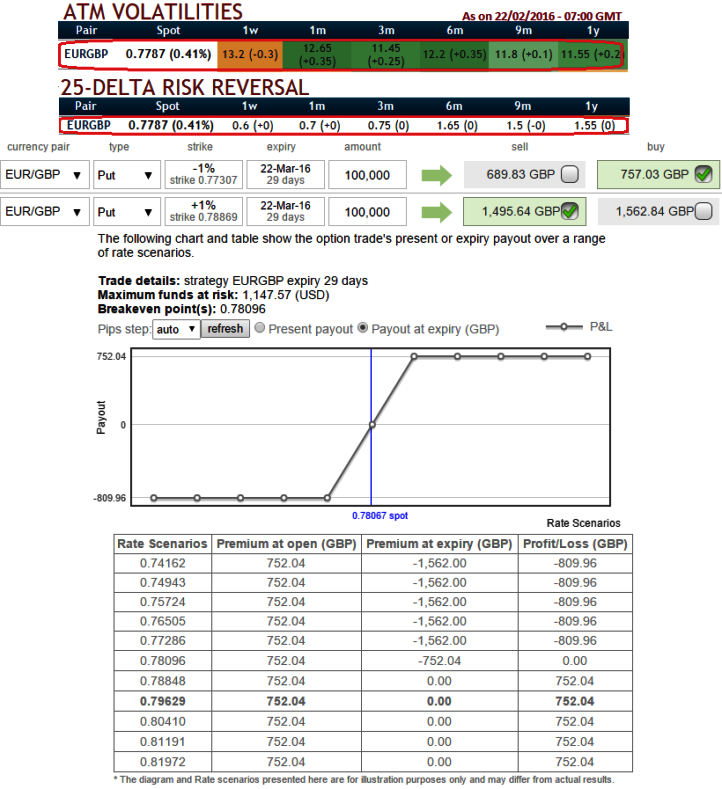

The implied volatility of ATM contracts for 1M-3M expiries of this the pair is flashing at around 12%.

Delta risk reversals creeping up gradually with positive numbers to signify the hedging positions are well equipped for upside risks over the period of time. While current IVs of ATM contracts are at higher levels but likely to perceive hover around 12% in long run.

In the FX option market, prices are quoted for standard moneyness levels for different time to expiry periods. These standard moneyness levels are At the money level, 25 delta out of the money level and 25 delta in the money level (75 delta) .

Since out of the money levels are liquid moneyness levels in the options market, market quotes these levels as 25 delta call and 25 delta put . If a trader has the right model, he can build the whole volatility smile for any time to expiry by using the three points in the volatility surface.

Hence, comparing this difference with implied volatility, OTC market sentiments and in options premiums we think the hedging costs for upside risks would be economical as result of deploying ATM instruments.

Now if you think speculation in potential uptrend in short terms is not possible as delta risk reversal suggested calls have been overpriced then let's look at an example and a few specific scenarios with alternatives in order to get benefitted from upswings.

Hedging Frameworks:

At this point of time, if you expect that EURGBP will mildly spike up over the next fortnight or so, spot FX is currently at 0.7812. And if you think calls are priced in expensive, then buy 1M (1%) Out of the money -0.37 delta put option. Simultaneously, short 1W (-1%) in the money put with positive theta, So thereby our breakeven would be at 0.7568.

Please be noted in this instance that the put we bought is out of the money and the put we sold is in the money with an anticipation of EURGBP could rise or remain unchanged, and there onwards any abrupt fall would be taken care by longs in OTM put and your active longs in spot FX would be protected.

Maximum profit: The initial credit received for this trade, less commission costs.

The maximum risk is the difference between the two strike prices, minus the credit you received.

Doubling leverage spread:

We see no divergence in spot FX with risk reversals, relying on the OTC hedging set up, aggressive bulls can prefer "Call Doubling Spread" that consists of buying a call of EURGBP at the money strike and buying another call at a higher strike price within same expiry.

Spread ratio: (1:1)

Call Double Construction: Initiate long in 1M at the money +0.51 delta call, initiate another long in 1M (1%) out of the money +0.39 delta call for net debit.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: EUR/GBP stagnant IVs and positive RR signal euro gains - bull spreads for risk averse and doubling spreads for aggressive bulls

Monday, February 22, 2016 10:27 AM UTC

Editor's Picks

- Market Data

Most Popular