Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

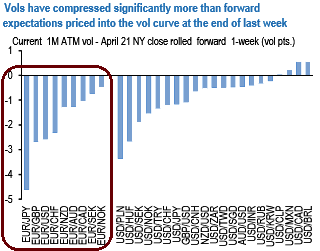

Well anticipated French election outcome on April 24th saw vols fall meaningfully below 1-day forward levels from last week’s close. Even adjusting for the sharp decline baked into forward vols to account for the passage of event risk, FX vols are materially lower than ex-ante forward roll expectations (chart 1).

The risk premium squeeze owes not only to a no-drama first round outcome, but also reduction of forward-looking expectations of a surprise from the 2nd round vote on May 7th with the market now more sanguine about the accuracy of opinion polls showing Macron with a 20-point lead over Le Pen.

Overnight vol for the second round vote in EURUSD, for instance, has fallen from 40 to 24 over the past week; EURJPY (-28 pts.), EURGBP (-17 pts.) and USDJPY (-11 pts.) have all suffered meaningful day-weight declines.

There is some, albeit limited room to chase front-end EUR options lower after this compression. 1M ATMs may have 0.5-1.0 vol to subside to converge to realized vols, which themselves are likely to fall as the initial euphoria gives way to a period of deliberation and consolidation during which the market absorbs the ECB’s dogged cautiousness on inflation.

The flatness of the 2M-1M vol curve is at odds with the mildly upward sloping vol curve elsewhere say in USDJPY and USDCHF, and is unsustainable in an environment of narrowing risk premia, hence we tactically sold 1M 25D EUR put strikes in long/short RV against JPY gamma.

Please be noted that the above nutshell evidencing delta risk reversal numbers are flashing up higher negative prints to indicate the mounting hedging interests for bearish risks. 25-delta risk reversals would imply that the difference in volatility, and therefore price, between puts and calls on the most liquid out-of-the-money (OTM) options quoted on the OTC market. Negative value also implies puts are more expensive than calls (downside protection is relatively more expensive).

However, EUR-cross-risk-reversals have understandably re-priced sharply in the direction of EUR calls, especially against G10 commodity currencies that were among the worst performers on the week. We struggle to see severe dislocations in this space at current levels, with some mild value only in EURCAD 3M riskies at 0.4 which we are not inclined to chase in light of the cheapness of the loonie on short-term models and the potential for an oil rebound in coming weeks that can cap the extent of EURCAD strength. EURCNH riskies (3M 25D -0.05) however strike us as interesting buys.