FxWirePro: NZD/USD retreats as Middle East instability weighs

FxWirePro: NZD/USD retreats as Middle East instability weighs  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  FxWirePro: USD/JPY holds tight range ahead of key U.S. payrolls data

FxWirePro: USD/JPY holds tight range ahead of key U.S. payrolls data  FxWirePro: GBP/AUD eases slightly, focus on near-term support

FxWirePro: GBP/AUD eases slightly, focus on near-term support  FxWirePro : USD/CAD falls as strong Canadian jobs data lifts loonie

FxWirePro : USD/CAD falls as strong Canadian jobs data lifts loonie  FxWirePro: EUR/AUD slips after surprise U.S. employment data

FxWirePro: EUR/AUD slips after surprise U.S. employment data  AUDJPY Bears Poised: Sell Rallies at 111.55 for 108 Target with 112.20 Stop

AUDJPY Bears Poised: Sell Rallies at 111.55 for 108 Target with 112.20 Stop  FxWirePro: AUD/USD eases as investors await U.S. employment figures

FxWirePro: AUD/USD eases as investors await U.S. employment figures  FxWirePro: USD/CNY slips as strong China exports data Lift yuan

FxWirePro: USD/CNY slips as strong China exports data Lift yuan  EURGBP Bears Break Trendline: Sell Rallies at 0.8578 as Support Breach Eyes 0.8450 Slide

EURGBP Bears Break Trendline: Sell Rallies at 0.8578 as Support Breach Eyes 0.8450 Slide  EUR/USD Rockets Past 1.1560 as Soft U.S. Jobs Data Fuel Fed Rate-Cut Surge

EUR/USD Rockets Past 1.1560 as Soft U.S. Jobs Data Fuel Fed Rate-Cut Surge  FxWirePro: USD/ZAR gains some ground, but downtrend remains

FxWirePro: USD/ZAR gains some ground, but downtrend remains  FxWirePro: EUR/ AUD neutral in the near term, scope further downside

FxWirePro: EUR/ AUD neutral in the near term, scope further downside  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  FxWirePro- Woodies pivot (Major)

FxWirePro- Woodies pivot (Major)  Bitcoin Reclaims $65,000 as Easing Geopolitical Tensions Fuel Risk-On Rally

Bitcoin Reclaims $65,000 as Easing Geopolitical Tensions Fuel Risk-On Rally

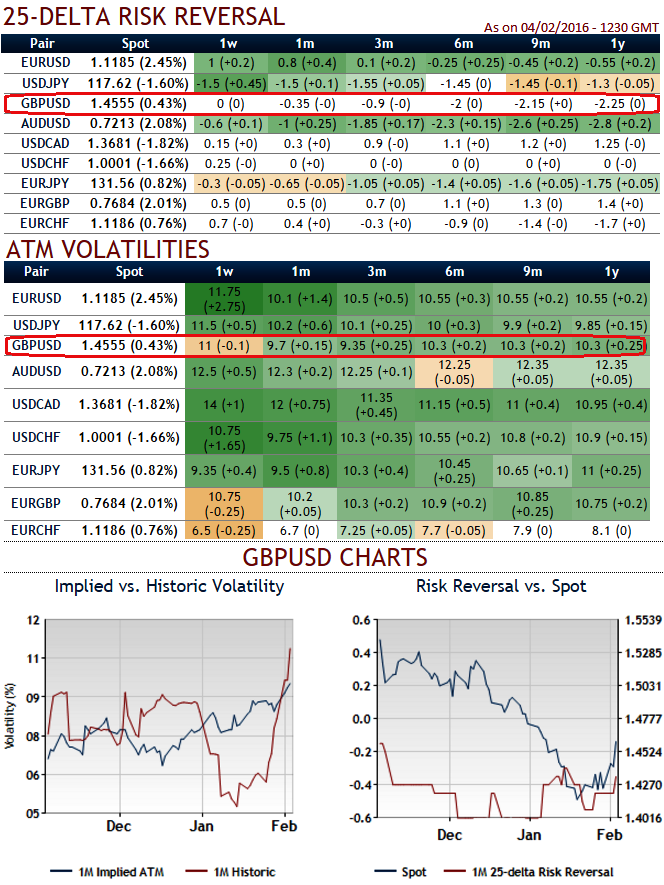

GBP vols ahead of UK Brexit risk: suspicious but not panicky The eruption of Brexit threats on the GBP vol scene can be traced in delta risk reversals. Way back in October and November even though 3M ATM IVs were tepid but tend to increase in the fears of Brexit pressures, during that period, while our aggregate VXY G7 FX vol index dropped -0.5vols, 3M GBP/USD vols spiked up +1.0vols.

But for now, OTC hedging arrangements for downside risks are intensifying 3M IVs have been reducing.

That a referendum on UK exit would take place in the near future was always a known fact since the Conservative Party won the General Elections. PM Cameron's letter to the European Council on Nov 10 and subsequent political declarations brought concerns surrounding UK exit from the EU to the forefront of investors' preoccupations and crystallized the expected referendum schedule around the summer 2016 - as evidenced by a historic steepening in GBP FX vols in the 6M-9M range.

The vol price action in the beginning of the year was that of a more homogeneous vol rally, as market turmoil fueled by global growth concerns, China woes and the extension of the commodities sell-off has lifted vols across the board.

A synthetic measure of GBP/G10 vols is currently back to levels last seen around the Jan 2015 SNB de-peg and ECB QE spell of volatility. Since the YTD FX vol rally is a generalized one, GBP vols do not stand out in particular, and Brexit fears are diluted within the generalized rise in risk premia. It is not yet the case that vols in GBP crosses are at extreme levels, especially given the disruptive nature of a Brexit scenario.

There is much more risk embedded in GBP risk reversals by comparison, as current aggregate levels of GBP RRs are overtaking the extremes of the pre-Scottish referendum scare and the UK General Elections, and match the summer 2011 sell-off episode.

While there hasn't been a formal announcement on the actual date, media reports have cited officials mentioning a 16-week period necessary to organize the referendum once a deal is worked out with the EU, which PM Cameron expects to happen at the Feb 18-19 meeting. This does make June a clear possibility, but a delay to September is very likely as well.

For now, we would still recommend a GBP/USD 3M risk reversal i/o 1Y as a generic hedge for Brexit risk. The ideal entry point is not ideal given the near doubling of the risk reversal since early October, but the bias is for further widening of the skew in 1H on slow-bleed demand for event protection.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: GBP baffles in OTC on Brexit speculations, which one would you rely upon IVs or risk reversals?

Friday, February 5, 2016 11:00 AM UTC

Editor's Picks

- Market Data

Most Popular