Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war  Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning  Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

The lira continued to weaken from the toxic combination of:

The rising US treasury yields and stronger USD

Turkey's diplomatic woes surrounding the US, and

The President Recep Tayyip Erdogan's renewed push for lower lending rates in the banking sector. In the latter context, Erdogan highlighted during a parliament speech recently that monetary conditions and access to loans have improved recently, despite resistance from the banks.

CBT held its MPC meeting today: The benchmark interest rate in Turkey was last recorded at 8 pct. Whereas the government is pushing ahead with measures to lower the lending rates of banks, in particular at state-owned banks - within this environment, a rate hike by CBT going forward seems exceedingly unlikely. The Central Bank of Turkey held its benchmark one-week repo rate at 8 pct.

On the contrary:

1) Core inflation has reached double-digit and shows no sign of calming down;

2) The trade deficit is widening out once again because of stronger import demand and higher oil prices;

3) The lira is weakening again - this is because higher inflation has lowered the real interest rate, while global bond yields are, in fact, rising.

At one point earlier this year, it appeared that the lira had stabilized; that core inflation might decelerate towards 9% - given that the weighted average cost of funding was around 12%, the prospective real interest rate had risen to a healthy c.3%. But, once core inflation is 11%, the real interest rate is back down at 1%.

We have experienced numerous times in recent years that this level does not support the lira when global yields are rising and EM risk appetite is reversing, which is the case now.

As a result, USDTRY has broken out to the topside recently; inaction on the part of CBT will only exacerbate this trend.

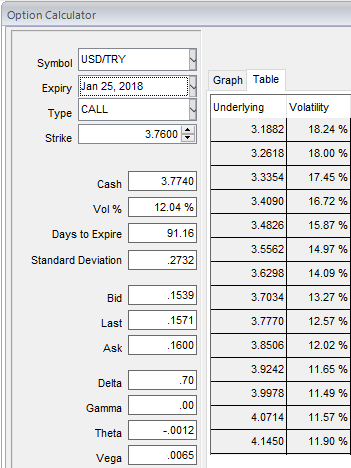

Yesterday, USDTRY traded up to 3.8080 on the onset of the news and retraced to 3.7210 currently. Buy the tail: Relative to recent history, implied vol and risk reversals are not high. Current 3m implied vol (12.5) could spike to the 16-20 area if accelerated depreciation did occur, while risk reversals could easily rise by 1-2 vol points.

Turkish lira implied volatility and risk reversals are among the highest in emerging markets. However, relative to recent history, they are not high in their own right.

Current 3m implied vol (12.04) could spike to the 15-16 area if accelerated depreciation did occur, while risk reversals could easily rise by 1-2 vol points.

This lends itself to owning volatility, and given the difficulty in ascertaining the probabilities of a “spike followed by a recovery” versus a “trend” move higher in USDTRY, we prefer a one-touch structure over a European digital. Hence, buying USDTRY 3m one-touch knock-in 4.25 has been advocated.