Part II — The listing: NFTs as bottle-stamps, and a vault the family is in no rush to sell

Part II — The listing: NFTs as bottle-stamps, and a vault the family is in no rush to sell  Economic pessimism has set in – but there are reasons for Australians to be hopeful

Economic pessimism has set in – but there are reasons for Australians to be hopeful  Open-Source AI Models Gain Ground as Enterprises Seek Lower-Cost Alternatives, Citi Says

Open-Source AI Models Gain Ground as Enterprises Seek Lower-Cost Alternatives, Citi Says  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  The government is ‘doubling down’ on its social media ban. But bigger penalties for platforms aren’t enough

The government is ‘doubling down’ on its social media ban. But bigger penalties for platforms aren’t enough  Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer

Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer  Despite its best efforts, Iran won’t be able to toll the Strait of Hormuz. Here’s why

Despite its best efforts, Iran won’t be able to toll the Strait of Hormuz. Here’s why  Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns

Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns

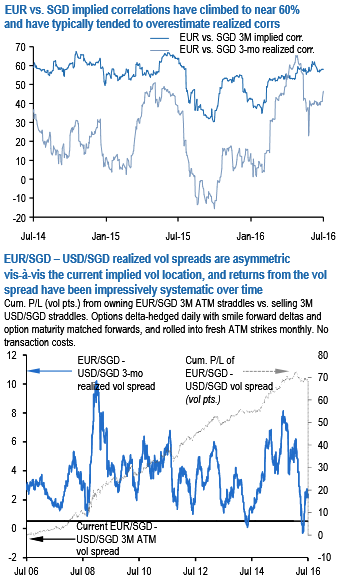

Long EUR/SGD vs. short USD/SGD gamma spreads form a classic relative value set-up with excellent entry levels, asymmetric payout profile and a long history of return outperformance. EUR vs. SGD implied correlations have recovered smartly from their Q1 lows towards 60%, and odds are that future realized corrs will fall short of this high bar as they have usually done in years past.

A direct corollary of this correlation set-up is that EUR/SGD – USD/SGD implied vols have fallen to multi-year lows, from where returns on the gamma spread are biased asymmetrically higher given the recent as well as the long run history of realized vol behavior (see chart).

The above chart also best reflects the persistent underperformance of EUR vs. SGD correlations in the form of impressive Sharpe Ratios from owning EUR/SGD vs. USD/SGD straddle spreads, indicating a degree of structural underpricing of EUR/SGD cross vols that is also shared by EUR-cross vols against other regional currencies such as KRW and INR.

While the precise cause is unclear, vega-supplying retail structured products might have a role to play in this, not dissimilar to the effect of higher profile Uridashis on JPY-cross vols spread is net time decay positive, and offers exposure to the idiosyncratic risk of INR volatility stemming from the RBI governor change and the specter of FCNR outflows.