Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations  Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate

Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate  Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

The UK has been entering a phase of relative growth underperformance.

A stronger global backdrop is benefiting the UK, prompting us to revise up 2017 GDP growth this week.

But the fundamentals driving domestic demand continue to look weak, particularly household real income.

We hence expect weaker consumption to slow UK growth relative to its trading partners this year.

We expect a shift to sub-trend growth this year will dissuade the BoE from raising rates.

This part of the forecast is the most uncertain. The UK saving rate had already looked low on the basis of historical UK experience and international comparisons. But the further decline from 6.1% to 3.3% during 2016 raises a question of sustainability.

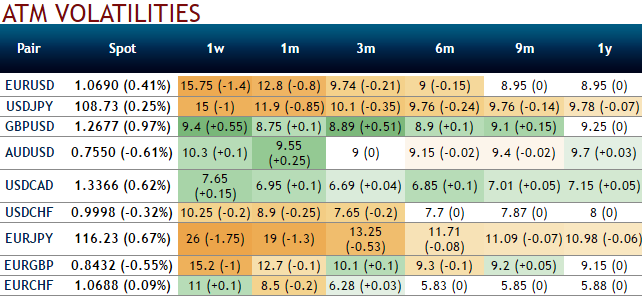

Please be noted that the risk reversals, for now, have taken adverse directions from last 1 year’s hedging sentiments that were bidding for upside risks.

While spiking IVs towards 9% for 1-3m tenors (for GBPUSD) 12.7% and 10% for the same tenors (for EURGBP) and, this volatile OTC market operations are due to the fact Eurozone elections are lined up signify hedging arrangements for upside risks over the period of time.