Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow

BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist

Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist  ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus

ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

The key driving force of loonie remains the relative priced pace of policy normalization. The conjecture behind a partial retracement higher in USDCAD is the expectation that relative monetary policy pricing will converge somewhat in the coming quarters. Post the June/July repricing, BoC is now priced to hike 67bps in two years, compared to the 32bp priced for the Fed, which in other words anticipates the policy rate spread (currently 39bp) to disappear.

This current differential in expected pace of policy normalization appears largely due to differences in policy reaction functions priced by markets: As much focus as there has been on US disinflation, Canada’s inflation recent undershoot is as nearly as severe and as surprising: the cumulative core undershoot is very similar for both (1.5% in Canadian core CPI and US core PCE, having declined 0.5 over the past 9 months).

Only a handful of the analysts polled by Bloomberg expect a further Bank of Canada (BoC) rate hike today. All others, us included, believe that it will leave its key rate unchanged at 0.75%. The market reaction to the rate decision is going to be more pronounced than analysts’ forecasts suggest, as the market is pricing in a rate hike with a much higher probability (above 40%). So if the BoC was to leave everything unchanged today, CAD is likely to ease notably.

While Canada’s unemployment rate has fallen swiftly in the past 12 months (-0.7%-pts) it has remained roughly in-line with developments in the US (0.6%-pts), and BoC’s assessment is that there remains slack in Canada, whereas US is now well under NAIRU estimates.

While the US normalization cycle is well further along, historically Canadian rate cycles have lagged US ones and peaked at lower rates; In the past 20 years US-CA 2y spreads have never been negative in a tightening cycle (currently 7bp). A sustained narrowing of yields might be more convincing once the Fed does near the end of its tightening cycle, while BoC is still in the middle of its own. This is more likely to unfold after mid-18 and for that reason, and because of a projected 2H18 bounce in crude oil prices, we have CAD rebounding some to 1.30 in fresh 3Q’18 targets.

In particular, as its inflation outlook is based on stable exchange rates, but CAD is trading almost 6% above the level assumed by the BoC. Excessively aggressive rate hikes would risk an overshooting of the exchange rate.

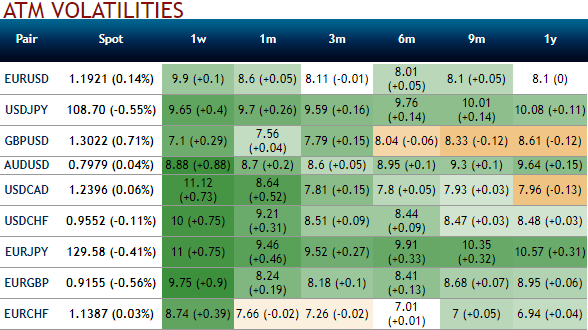

While the implied volatility remains among the three lowest G10 vols, seemingly options globally inexpensive. Despite the recent CAD appreciation, the USDCAD realized volatility has remained muted due to the low realized vol environment which makes knock-out barriers attractive.