Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

Euro area business and consumer surveys point to solid growth momentum in the region. Sentiment improved significantly during Q4’16 and remained robust in January. Consistent with this signal, Euro area GDP increased a solid 2% QoQ SAAR in Q4’16 and was revised up for Q3 in the flash GDP report, published almost two weeks ago.

In Eurozone, the consumer confidence printed at -4.9 in Jan which is a high dating back to early 2015. Consumer confidence gained some momentum in late 2016 after a poor start to the year and a downturn around Brexit. Though recent GDP and manufacturing surveys have been more positive, given the ongoing political uncertainty that foreshadows 2017, it is difficult to see the index strengthening much further.

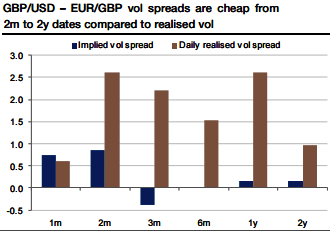

EUR risk prompts to pick the 6m tenor via volatility, the spread is the cheapest on the 3m and 6m tenors (see above graph). 3m contracts now encompass the French presidential election. We expect volatility disruptions ahead of the risk event to be potentially significant but short-lived.

All in all, a short-lived volatile period will be more effectively diluted in selling that premium over a 6m rather than a 3m vol contract, via a larger number of fixings. However, this is still a tail risk, so we prefer implementing the trade via volatility swaps rather than variance swaps (more painful if the unity of the euro area crumbles).

Go long GBPUSD vs EURGBP 6m volatility swaps @ 0.3 vols, indicative offer; same GBP notional in both legs. The vega MTM is roughly proportional to the implied vol spread and its odds are even more attractive than the realized vol odds, which reflect the odds of the payoff at expiry (see distribution chart on above graph for realized vols).

Indeed, the trade valuation will benefit from any widening of the implied spread from its almost flat level (a March hike surprise would definitely shake cable more than EURGBP).

So we recommend unwinding the package in the event of early vega profit, especially if it happens before the French election.

Risk profile: A durable surge in EUR crosses vols, a spread of volatility swaps is exposed to the volatility differential between two currency pairs. Investors holding the position until the 6m expiry face unlimited losses if the realized volatility between GBPUSD and EURGBP goes below 0.3 vols.