Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX

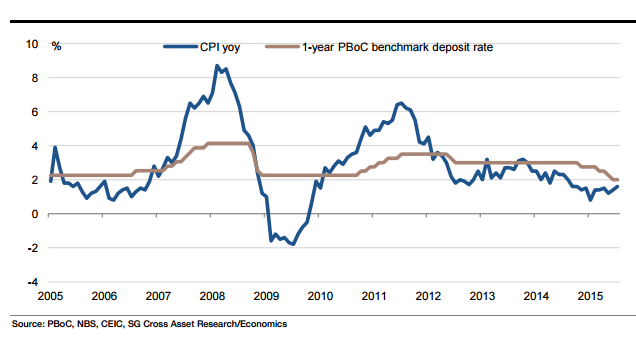

Given the supply shortage and the upcoming seasonal increases in pork demand, the pork prices will probably keep moving higher in the short term. Consequently, the CPI could be pushed higher. However, this pork cycle is not expected to go very far. First and foremost, there is little support from demand factors. In addition, the supply problem may not worsen much further since the government has beefed up its pork reserves following the painful lessons from previous episodes. Therefore, the CPI is expected to rise above 2% yoy in the coming months, but to peak around 3% yoy by year-end. This represents an upward revision to the previous forecasts: 1.9% yoy instead of 1.5% yoy for Q3 and 2.5% yoy up from 1.7% yoy for Q4.

This revision supports the current monetary policy call of no further policy rate cut this year. Currently, the 1-year benchmark deposit rate is at 2%. There are precedents that the PBoC cut policy rates when CPI was higher than this benchmark rate, but every time that happened CPI was already on a sharp downward trend. Since 2002, the PBoC has never cut policy rates when inflation rises for three consecutive months.

Judging from recent activity data, the economy is still under immense downward pressure. Furthermore, supply-driven inflation is by nature deflationary, as higher pork prices can squeeze other consumption in the absence of any acceleration in income growth. Therefore, fiscal policy has to step up, and monetary policy is likely to play an assisting role by providing targeted liquidity. It seems that the focus at the moment is on the indirect channels of policy bank funding support to infrastructure investment.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Rising CPI to limit PBoC’s scope for rate cuts

Monday, August 10, 2015 8:34 PM UTC

Editor's Picks

- Market Data

Most Popular