World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules

lures option holders on time decay merits - EconoTimes)

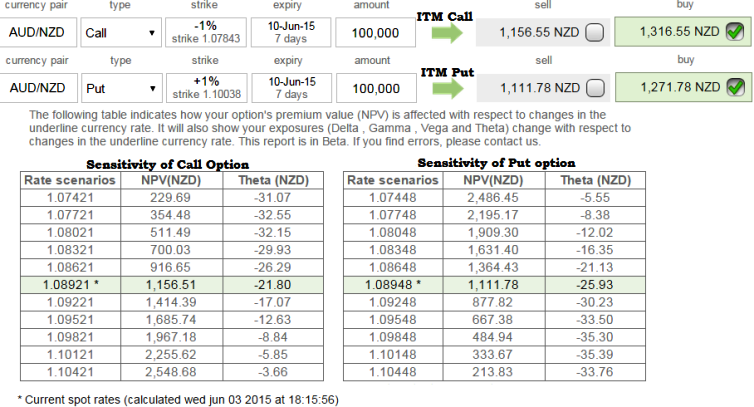

As shown in the nutshell, there is no significant change in theta value even though the underlying exchange rate oscillates dramatically. (From spot 1.0894, even if it moves to any extreme directions 1.1044 or 1.0744 then Theta is not turning into positives).

Here, Theta was in the range of -21.9 to -25.93 when the options value at execution NZD 1316.55 on Call & NZD 1271.78 on put respectively.

Theta has not been that sensitive to option's value to the passage of time.

For ITM call option, as time to expiry draws nearer, Theta lowers and decreases. In this case of AUD/NZD long guts, the relative change is not significant.

Option basket: Long Guts (AUD/NZD)

As we advocated this strategy in our earlier post, we remain firm and re-iterate often and often by stating that Theta on this strategy signifying time decay advantage of the ITM options of this pair as shown in the diagram.

The long guts is a neutral strategy in options trading that involve the simultaneous buying of an ITM call option and an ITM put option of the same underlying currency and expiration date.

This is an unlimited profit on either side, limited risk to the extent of premium paid. The position is taken when the options trader thinks that the underlying stock will experience significant volatility in the near term.

These long guts are a debit spread as a net debit is taken to enter the trade.

Large gains for the long guts strategy is attained when the underlying currency price makes a very strong move either upwards or downwards at expiration.

The move in the underlying currency price must be strong enough such that either the long call or the long put rise enough in value to offset the loss incurred by the other option expiring worthless.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Theta (Θ) lures option holders on time decay merits

Wednesday, June 3, 2015 1:08 PM UTC

Editor's Picks

- Market Data

Most Popular