How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done

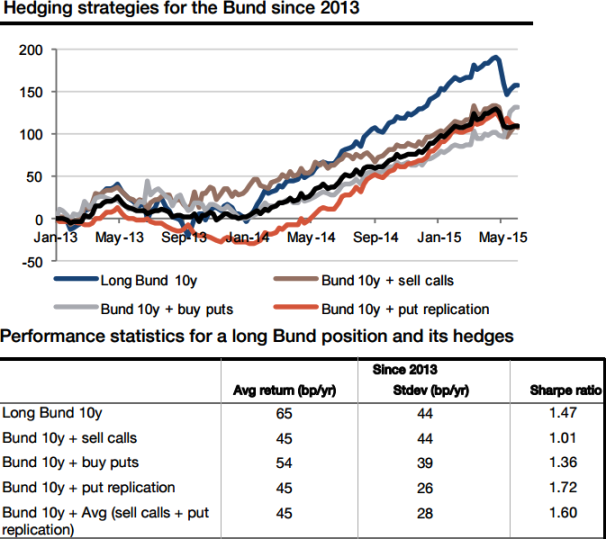

The timing of a rise in interest rate has been a double-crossing theme. Yet bond sell-offs arise, badly hurting fixed income and global macro portfolios.

What relief can be found in systematic strategies? To what extent does the premium paid for insurance against interest rate rises erode a fixed income portfolio performance?

The option market maker who sells options and hedges position on a regular basis as the trend follower is in the same position.

When the asset deviates from the strike and when the delta of its position increases, the option hedger will buy more of the underlying asset.

The graph demonstrates the total performance in bps equivalent (i.e. the gain in basis points) of an outright long position in 10y German Treasuries and the combination of this long position in 10y German Treasuries and one of the three systematic strategies given in the nutshell.

The black line indicates the performance for a long position in German Treasuries, combined with a put replication strategy and a programme selling receivers on 10y rates.

Here, in German bond market case, Gap risks such as the one witnessed in April/May will remain unhedged as the German bond yields have been performing well.

But the traders who are risk averse can still prefer any of the combined strategies according to the circumstances.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Trade laggards can deploy momentum strategies on German treasury bonds

Wednesday, June 10, 2015 6:53 AM UTC

Editor's Picks

- Market Data

Most Popular