Asian Stocks Mixed as Chip Selloff Hits KOSPI, Nikkei Ahead of US Jobs Data

Asian Stocks Mixed as Chip Selloff Hits KOSPI, Nikkei Ahead of US Jobs Data  Canada, US Hold Constructive Trade Talks as Tariff Negotiations Continue

Canada, US Hold Constructive Trade Talks as Tariff Negotiations Continue  US Dollar Falls as Weak July Jobs Report Dents Fed Rate Hike Bets

US Dollar Falls as Weak July Jobs Report Dents Fed Rate Hike Bets  FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  BOJ Rate Hike Expectations Rise Ahead of September Meeting

BOJ Rate Hike Expectations Rise Ahead of September Meeting  China Exports Beat July Forecasts as AI Demand Fuels High-Tech Trade

China Exports Beat July Forecasts as AI Demand Fuels High-Tech Trade  Asian Stocks Cautious Ahead of US Jobs Data as Oil Rises

Asian Stocks Cautious Ahead of US Jobs Data as Oil Rises  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Oil Prices Set for Steep Weekly Losses as Hormuz Deal Stalls

Oil Prices Set for Steep Weekly Losses as Hormuz Deal Stalls  China Inflation Cools in July as CPI Misses Forecast, PPI Deflation Eases

China Inflation Cools in July as CPI Misses Forecast, PPI Deflation Eases

International developments moved to the back seat this week, as the risks stemming from Greek debt crisis and China’s equity market eased off for now. However, renewed weakness in commodity sector and concerns over corporate profitability weighed on market sentiment.

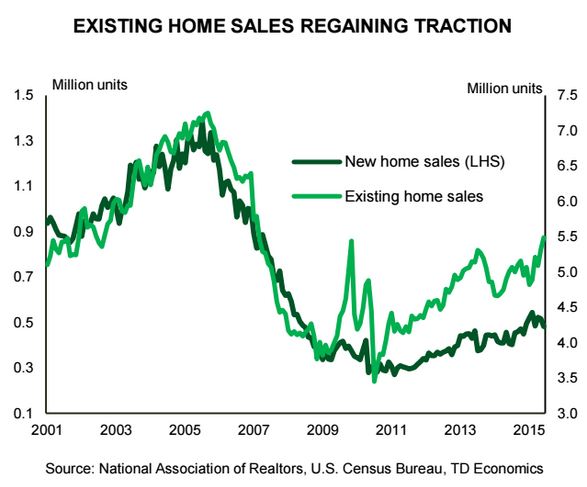

The domestic data flow remained relatively upbeat. Initial jobless claims fell to a multi-decade low. Existing home sales rose by 3.2% in June to a new cycle high. New home sales disappointed, declining by 6.8% in June, however they were still up 18% relative to a year ago.

Next week should bring further evidence of a rebounding economy, with second quarter GDP reading expected to show a 2.5% gain. The upturn in economic data is likely to be recognized in the Fed’s July interest rate announcement, which we expect to set the stage for September rate liftoff.