Canada-Indonesia Trade Pact Gains Momentum as Carney and Prabowo Discuss Economic Cooperation

Canada-Indonesia Trade Pact Gains Momentum as Carney and Prabowo Discuss Economic Cooperation  China Trade Surplus Surges in May 2026 as Exports and AI-Driven Imports Accelerate

China Trade Surplus Surges in May 2026 as Exports and AI-Driven Imports Accelerate  Morgan Stanley Upgrades Winbond and Nanya to Overweight on Strong Memory Chip Market Outlook

Morgan Stanley Upgrades Winbond and Nanya to Overweight on Strong Memory Chip Market Outlook  US-Iran Gulf Clash Raises Oil Market and Defense Stock Concerns

US-Iran Gulf Clash Raises Oil Market and Defense Stock Concerns  China’s Cross-Border E-Commerce Faces Rising Costs and Slower Growth in 2026

China’s Cross-Border E-Commerce Faces Rising Costs and Slower Growth in 2026  Vietnam Prioritizes Fiscal Stimulus as Monetary Policy Space Narrows

Vietnam Prioritizes Fiscal Stimulus as Monetary Policy Space Narrows  US Dollar Dips as Middle East Tensions Ease; Markets Await Key US Inflation Data

US Dollar Dips as Middle East Tensions Ease; Markets Await Key US Inflation Data  Fed’s Anna Paulson Signals Rates Could Stay Higher Longer Amid Inflation Risks

Fed’s Anna Paulson Signals Rates Could Stay Higher Longer Amid Inflation Risks  US Stocks Rebound as Iran Eases Military Operations; Tech Shares Lead Wall Street Recovery

US Stocks Rebound as Iran Eases Military Operations; Tech Shares Lead Wall Street Recovery  Gordie Howe International Bridge Set to Open, Boosting U.S.-Canada Trade Links

Gordie Howe International Bridge Set to Open, Boosting U.S.-Canada Trade Links  Gold Tumbles Below $4,400 on NFP Shock: Fed Easing Bets Crater, Sell on Rallies to $4,300

Gold Tumbles Below $4,400 on NFP Shock: Fed Easing Bets Crater, Sell on Rallies to $4,300  BOJ Governor Ueda Warns Oil Price Shock Could Trigger Persistent Inflation

BOJ Governor Ueda Warns Oil Price Shock Could Trigger Persistent Inflation  Gold Prices Hit 11-Week Low as Strong U.S. Jobs Data Dampens Rate Cut Hopes

Gold Prices Hit 11-Week Low as Strong U.S. Jobs Data Dampens Rate Cut Hopes

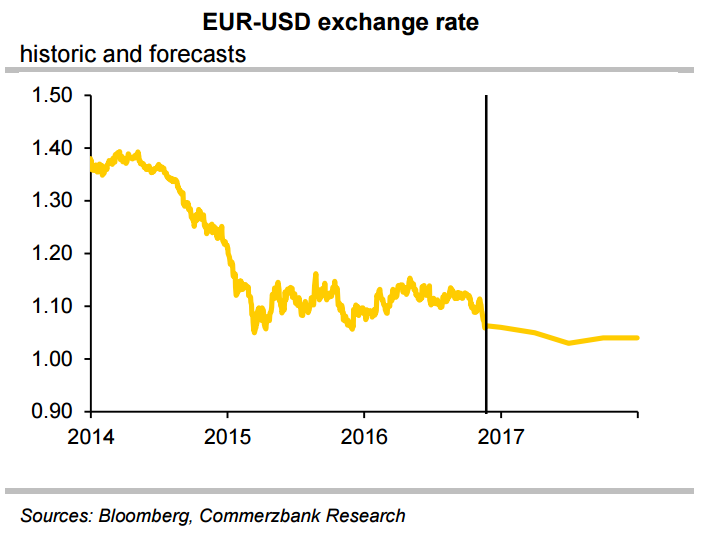

The European Central Bank (ECB) will decide on December 8 on whether and how to extend its 80 billion euros ($85 billion) monthly bond purchases and expectations are for the programme to continue beyond its current March deadline. Two of the top officials said earlier this week that the ECB needs to continue supporting the euro zone economy with its ultra-loose policy, cementing expectations for an extension of the ECB's bond-buying scheme next month.

Euro zone inflation was 0.5 percent last month and is expected to rise beyond 1 percent early next year, mainly due to a stabilisation in oil prices. However, the ECB is still a long way off its inflation target of almost 2 percent.

Analysts are not very hopeful that the economic environment or the core inflation trend in the eurozone will improve notably. President Mario Draghi also told a European Parliament committee on Monday the ECB needed to maintain its current level of monetary support to bring euro zone inflation back to its target.

"The ECB will be forced to get active again and will prolong the deadline of the asset purchases beyond March 2017 for another six months. Our experts do not expect another cut of the deposit rate, though," said Commerzbank in a report.

The US economy rose by a solid 2.9 percent q/q (annualised) in Q3 and the unemployment rate is lingering at 5 percent. Inflation stood at 1.5 percent y/y and the Fed’s preferred mean for core inflation, the PCE index, at 1.7 percent. Based on improving fundamentals, the Fed signalled an imminent rate hike at its October meeting. At its November meeting, he Fed refrained from hiking the key rate ahead of US presidential election on 8th November, but repeated the strong indication for a hike.

Donald Trump' victory has raised US interest rate expectations markedly. Trump's expansionary fiscal and protectionist trading policy are likely to boost the USD and drive up inflation. A rate hike in December is now almost fully priced in by markets. The market has also come to attach a likelihood of over 50 percent to two additional Fed rate hikes in 2017.

Fed will keep hiking interest rates whereas the ECB will stick to its expansionary stance. With Fed and ECB monetary policies diverging further, EUR/USD is likely to remain subdued. By end-2017 the ECB will be forced to gradually stop buying bonds as it will gradually run out of eligible assets. This should support the euro against the US dollar by the end of 2017.

EUR/USD was trading at 1.0620 at around 1210 GMT as markets await FOMC minutes due later in the NY session. At the same time, FxWirePro's Hourly USD Spot Index was at 32.9119 (Neutral) and Hourly EUR Spot Index was at 69.1643 (Neutral). For more details on FxWirePro's Currency Strength Index, visit http://www.fxwirepro.com/currencyindex