Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  JPMorgan Lifts Gold Price Forecast to $6,300 by End-2026 on Strong Central Bank and Investor Demand

JPMorgan Lifts Gold Price Forecast to $6,300 by End-2026 on Strong Central Bank and Investor Demand  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  BTC Flat at $89,300 Despite $1.02B ETF Exodus — Buy the Dip Toward $107K?

BTC Flat at $89,300 Despite $1.02B ETF Exodus — Buy the Dip Toward $107K?  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

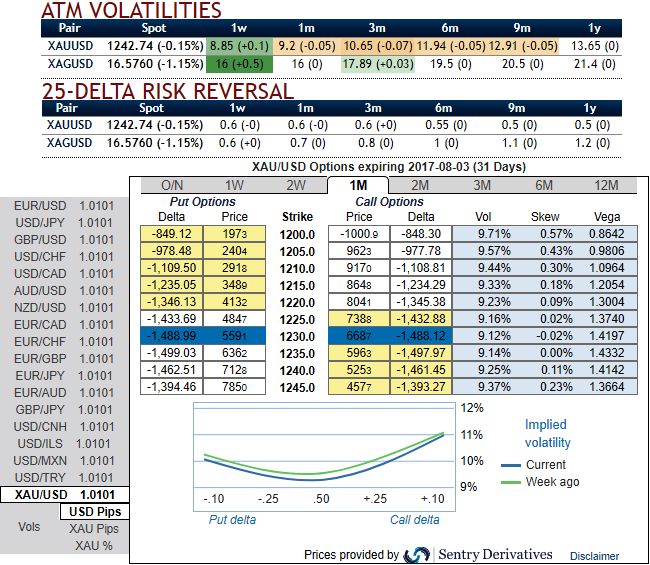

Gold price seems to be the consistent standout under an investor positioning mean reversion rule with a success ratio of over 60% over the last five years and modest average monthly returns, albeit with a low information ratio.

As our trade moved into the money, we tightened our stop to avoid a loss. Prices moved below this level on June 23 and we closed at a profit.

Yellow metal prices kept sliding and now is on the verge of two-and-a-half month lows today and were on track to post a third straight session of losses as a recovery in the dollar hit investor demand for the precious metal.

Comex gold futures were at $1,234.67 a troy ounce by 10.58 GMT, down $7.63, or around 0.62%. It was the lowest level since May 16.

In our recent write-up, we had advocated 3-way straddles versus OTM Calls, the short leg on call has worked out so far. For now, we would like to reshuffle the option strategy as shown below.

Option Strategy: 3-Way Options straddle versus put

Spread ratio: (Long 1: Long 1: Short 1)

The execution: Initiate long in XAUUSD 1M at the money vega put, long 1M at the money vega call and simultaneously, Short theta in 1m (1%) out of the money put with positive theta or closer to zero.Theta is positive; time decay is bad for a buyer, but good for an option writer.

Rationale: The nutshell showing delta risk reversals above explains that hedgers’ interests have been neutral but upside risks are lingering, however, no new shift in sentiments is observed. While positively skewed IVs are also well balanced to signal the swings likely to oscillate on either direction. You could now again observe ETF positions have also surged in the last quarter.

As a result, we don’t see much traction OTM calls. While 1m – 1y IVs trending lower towards 9.2% to 13.65%. A seller wants IV to shrink away so the premium falls. You should also note short-dated options are less sensitive to IV, while long-dated are more sensitive.

Hence, we encourage vega longs and short thetas in the non-directional trending pair but slightly favors bearish strategy as the vega signifies the sensitivity of an option’s value owing to a shift in volatility. It is usually expressed as the change in premium value per 1% change in implied volatility.