FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  BTC Flat at $89,300 Despite $1.02B ETF Exodus — Buy the Dip Toward $107K?

BTC Flat at $89,300 Despite $1.02B ETF Exodus — Buy the Dip Toward $107K?  Nasdaq Proposes Fast-Track Rule to Accelerate Index Inclusion for Major New Listings

Nasdaq Proposes Fast-Track Rule to Accelerate Index Inclusion for Major New Listings

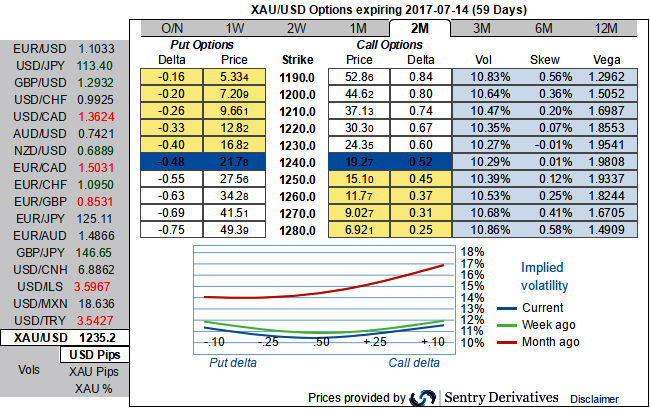

The above sensitivity tool evidencing delta risk reversals and IV skews evidence gold prices’ momentary edginess and upside risks in long run. Positively skewed IVs of 2m tenors indicates hedgers’ interests in both OTM put and call strikes, while neutral delta risk reversal number indicates topsy-turvy swings in this precious commodity prices.

Well, envisaging the short term range bounded trend and uncertain trend in long term from above OTC market’s rationale; we reckon that the calendar straddle would be more advantageous to keep price fluctuations on the check.

The strategy could be executed by shorting a near-term straddle while buying a longer term straddle with an intention to profit from the rapid time decay of the near-term options sold.

Well, it is a limited return with the limited risk strategy entered by the options trader who ponders over that the underlying spot commodity price would experience very little volatility in the near term (please refer above nutshell).

Execution: Stay short in ATM call and ATM put of 1m expiry, while simultaneously buy 6m +0.51 delta call and -0.49 delta put of the similar tenor at net debit.

Maximum loss for the calendar straddle is limited and is likely incurred when the spot price had moved hugely in either direction on the expiration of the near-term straddle.

Maximum gains for the calendar straddle are earned when the gold prices are trading at the strike price of the options sold on the expiration of the near-term straddle. At this price, both the written options expire worthless while the longer term straddle being held will suffer only a small loss due to time decay.