Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis

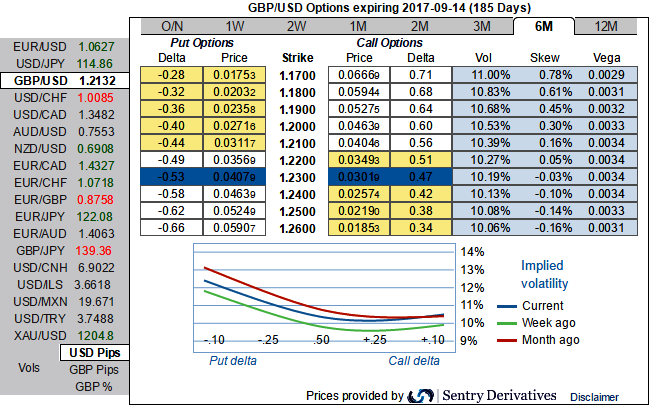

GBP is the second worst-performing currency over the past two weeks as evidence cumulates of a broad-based loss in economic momentum(the TWI has lost 3%to 1% below the 6m average). The economy was a support for GBP through H2’16 as growth accelerated rather than slowed following the Brexit vote, helped by the easing in financial conditions.

But with growth on course to slow by more than half from the 2.8% recorded in Q4’16 as consumers feel the pinch from inflation and business capex remains weak, GBP is being undermined by a pronounced deterioration in interest rate support.

The deterioration in the UK data cycle could not have been more poorly timed for GBP as

1) It contrasts with acceleration in global growth, and

2) The Brexit process will soon begin in earnest as the UK government is close to securing parliamentary assent for Article 50 (the House of Lords attached two amendments to the Brexit Bill but the Commons is expected to reject these). It should become apparent fairly soon during the formal exit negotiations which follow that the UK is headed towards a harder Brexit outside the single market as Europe is not willing to compromise the EU’s principle freedoms while the UK will not compromise on a desire to control migration. A possible second Scottish referendum can be added to GBP’s Brexit woes (the SNP conference is March 17-18).

All these fundamental driving forces of GBPUSD are factored in OTC FX markets.

The negative delta risk reversal numbers are bidding for downside risks, while IV slews are also substantiating this stance as the hedgers' interests are stretched towards OTM put strikes.

While risk reversals of 6m tenors also indicate the high degree of bearish risks, this would imply that the puts are relatively costlier than the call options, while 6m IV skews are the evidence of the hedgers’ interests of OTM put bids.