UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  JPMorgan Lifts Gold Price Forecast to $6,300 by End-2026 on Strong Central Bank and Investor Demand

JPMorgan Lifts Gold Price Forecast to $6,300 by End-2026 on Strong Central Bank and Investor Demand  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch

If you could observe from the technical charts of NZDJPY in the recent past, it has shown a considerable resilience, (observe bearish candles with big real bodies of previous months, refer above technical chart), we continue to foresee the same in next two days’ time.

Before describing the Vega longs, let’s begin with volatility.

The volatility of any asset price (NZDJPY currency pair in this case) is simply how much it fluctuates with no regard to direction. A higher volatility means the price has moved or is expected to move over a larger range in a set time period.

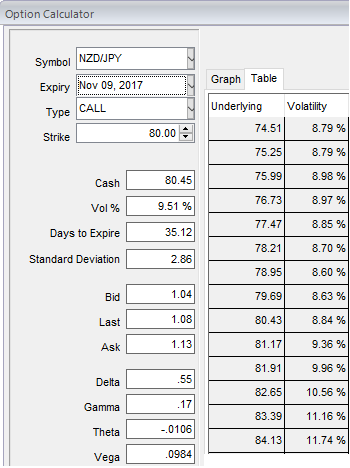

Please be noted that the implied volatility of the 1m call options of NZDJPY is trending higher at 9.5%.

Future volatility is the volatility of the underlying price over some period in the future. The price of an option depends on future volatility, yet it is impossible for anyone to know exact future volatility. However, it is possible to calculate the market place’s expected future volatility using the option’s price itself. This is known as implied volatility (IV).

Vega longs are contemplated in this strategy as it measures the sensitivity of an option’s value to a change in volatility. It is usually expressed as the change in premium value per 1% change in implied volatility.

Well, in order to arrest the puzzling swings that are lingering in intermediate trend and prevailing declining trend, we recommend diagonal option strap strategy that favors underlying spot’s upside bias in long run and mitigates bearish risks in short term.

So, we recommend building the FX portfolio exposed to this pair with longs positions in 2 lots of 1M ATM 0.51 delta calls and 1 lot of ATM -0.49 delta puts of similar expiries, the strategy is constructed at the net delta of 50%.

This NZDJPY strategy should take care of both upswings and downswings simultaneously, and on speculative grounds, the strategy is likely to derive handsome returns on the upside and certain yields regardless of swings on either side but with more potential on the upside, thereby, one can achieve trading or speculative objective.

Straps are likely to render buyer the right to buy underlying spot FX at predetermined regardless of the trend with the limited risk to the extent of initial premium paid, this strategy is used when the options trader ponders over the underlying spot price would sense significant volatility which seems most likely ahead of central bank events as stated above.

FxWirePro launches Absolute Return Managed Program. For more details, visit: