Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields  US Inflation Expected to Ease in June, but Fed Rate Hike Risks Persist Amid Middle East Tensions

US Inflation Expected to Ease in June, but Fed Rate Hike Risks Persist Amid Middle East Tensions  Morgan Stanley Downgrades Adobe, Workday as AI Transition Raises Growth Concerns

Morgan Stanley Downgrades Adobe, Workday as AI Transition Raises Growth Concerns  UBS Boosts China Tech Bets, Adds Kuaishou and Meituan to Focus List

UBS Boosts China Tech Bets, Adds Kuaishou and Meituan to Focus List  ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus

ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus  BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning

BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning  Fed Chair Kevin Warsh Launches Task Forces to Overhaul U.S. Monetary Policy Framework

Fed Chair Kevin Warsh Launches Task Forces to Overhaul U.S. Monetary Policy Framework  RBNZ Raises Interest Rates to 2.50%, Signals More Tightening as Inflation Risks Persist

RBNZ Raises Interest Rates to 2.50%, Signals More Tightening as Inflation Risks Persist  Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt

Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt

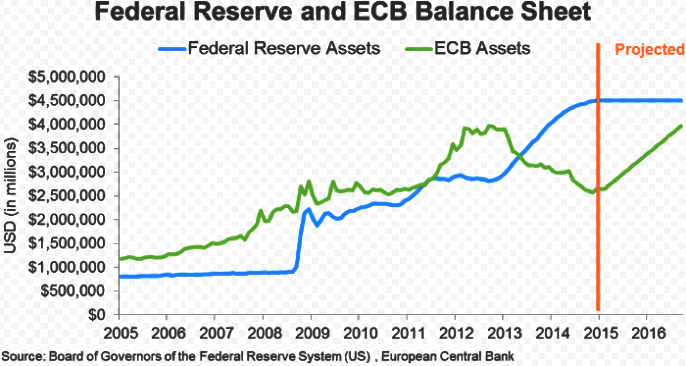

Last month of 2015, the ECB has not delivered what streets expected (not a full depo cut we had in mind i.e. -10bps versus forecasts of -20bps) but the extended QE programme we were looking for (now due to run at least until March 2017).

Slow pace of easing: The ECB has been firm for a programme of reinvestment as existing holdings mature, while many expected the expansion pace of asset purchases.

Although Draghi claims the reinvestment will add EUR 680bn to the ECB's balance sheet by 2019, it is perceived that he disappointed to a market accustomed to, (1) upfront easing and (2) Draghi over-delivering.

It is clear he had no consensus to be much more aggressive, even though promises by Draghi that further monetary stimulus could be underway, many analysts are skeptical on central bank's sizable additions to its €1.46 tn asset-purchase programme in 2016.

There were rumors of a marginal of nonconformity by eidmann/Lautenschlaeger as well as Knot/Hansson/ Rimsevics though note Weidmann and Lautenschlaeger (the two German members) are also said to have opposed the original QE announcement in Jan.

Draghi himself says "it may take years" before the EZ returns to pre-crisis unemployment rates, but "as we have seen in the UK and US, event at that point... there may still be a substantial time lag before a tight labor market translates into higher wages."

Conversely, the first Fed rate hike is finally behind us. Many were calling for a "dovish hike" but relative to already very dovish expectations, this was nothing of that sort.

FOMC members' economic projections still imply four more hikes next year, well ahead of what the market is priced for. For many, the 25% rally in DXY to its Dec peak is likely to mark the exhaustion of the trend.

However, these speculations have left the forecasts unchanged in this month (EUR/USD 1.03 end-Q1 and parity by end-Q2).

Hence, EURO could be boosted temporarily by risk aversion in its role as risk off proxy or more sustainably by signs of inflationary pressures.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

ECB’s B/S numbers despite German members’ denials to prop-up EURO while Fed’s hiking in 2016 likely to trim EUR/USD

Monday, January 4, 2016 11:41 AM UTC

Editor's Picks

- Market Data

Most Popular

7