BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning

BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning  Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist

Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist  Gold’s Bull Run Intact: Safe-Haven Bids Overpower Treasury Yield Pressure

Gold’s Bull Run Intact: Safe-Haven Bids Overpower Treasury Yield Pressure  Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions  BOJ Rate Hike Expectations Rise Ahead of September Meeting

BOJ Rate Hike Expectations Rise Ahead of September Meeting  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation  Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

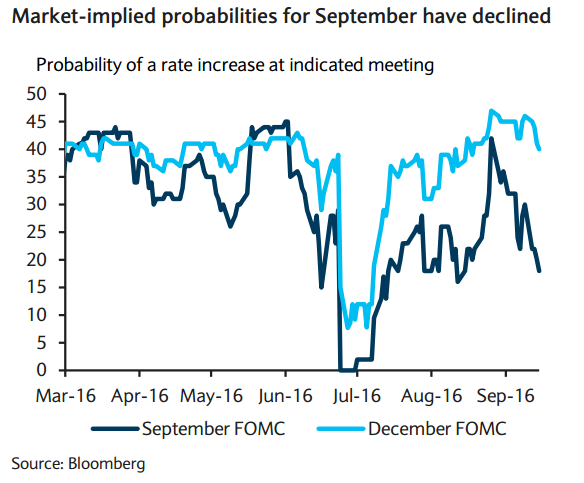

The probability the market attaches to a rate rise at FOMC decision due Wednesday now stands at just 20 percent. While the recent run of US economic data has reduced the likelihood of a rate hike at Wednesday’s meeting, the focus will be on Fed Chair Yellen’s conference and the signals that the FOMC send around the prospect of a rate hike before year-end.

The FOMC kept its target policy range for the federal funds rate unchanged at 25-50bp at its June and July meetings and all FOMC participants expected at least one rate hike in 2016. Incoming data since mid-year have generally improved and external risks have diminished. Communications from many FOMC members also indicate a willingness to prepare markets for the next rate increase.

The inflation data have evolved generally in line with the Fed’s forecasts, pass-through effects are clearly fading. "If Fed officials were focused only on the employment situation, the probability of tightening in September would be high. However, inflation is also a key consideration, and the latest data argue for patience," said Daiwa Capital Markets in a report. The consumer price index showed a hint of pressure in August, but much of the upside surprise seemed to reflect random volatility.

The July reading on the price index for personal consumption expenditures was well contained, with the headline index showing no change and the core component increasing only 0.1 percent. The restrained nature also was evident in the Dallas Fed's trimmed mean PCE price index, a measure frequently mentioned by Fed officials. This index rose less than 0.1 percent in July, which pushed the annual inflation rate back to the low portion of its recent range.

Fed most likely on hold in September and is likely to remain on the sidelines in November because of the upcoming presidential election. Many market participants are shifting their focus to a potential change at the FOMC meeting on December 13-14. Assuming policy is left unchanged, from a market perspective, the reaction is likely to depend on the tone of the accompanying statement and forecasts, and the extent of any dissent.

The greenback remains on the defensive against its main rivals on Monday. The dollar index was down 0.14 percent at 95.91, EUR/USD was up 0.08 percent at 1.1158 and USD/JPY down 0.36 percent at 101.86 at around 11:50 GMT.