How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform

How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform  Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940  Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring

Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring  Same sparkle, different story: how lab-grown diamonds are transforming the market

Same sparkle, different story: how lab-grown diamonds are transforming the market  Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be  3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online

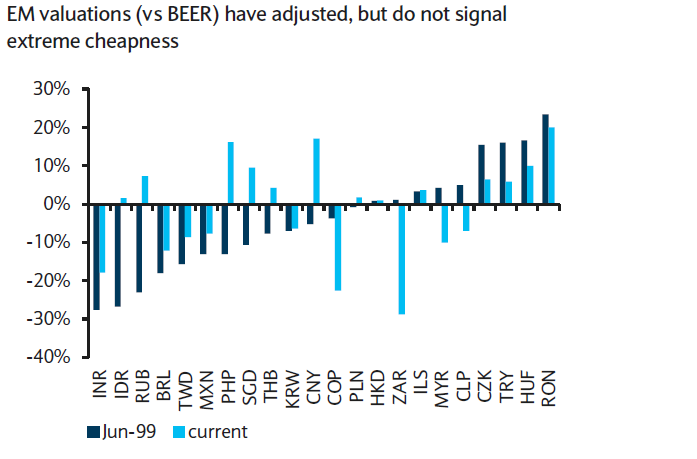

Although some currencies have weakened sharply due to global slowdown especially China, all EM FX do not appear to have overshot. EM Asia FX will face the brunt of slowing Chinese growth and a weaker CNY. Korea and Taiwan are particularly vulnerable given their general openness to trade and their trade exposure to China.

In addition, Korea is actively looking to recycle its current account surplus while having less room to boost economic conditions via policy easing. In Taiwan, exports have been weak recently and could face further pressure from slowing growth in China.

While Elsewhere in EM corporate, we think Hong Kong issuers are likely to benefit from the outflows triggered by a change in China's FX policy. Liquidity and deposits in Hong Kong banks are likely to increase substantially, creating a bid for the bonds they typically buy.

We recommend buying 6 month USDKRW and USDTWD NDFs. We have also initiated a long USDCNH 6m forward recommendation as forwards are not pricing in the extent of weakness in CNY/CNH.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FXWirePro: Korea capitalizing trade surplus despite Chinese slowdown – 6M forwards for hedging

Tuesday, September 29, 2015 1:24 PM UTC

Editor's Picks

- Market Data

Most Popular