Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns

Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer

Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer

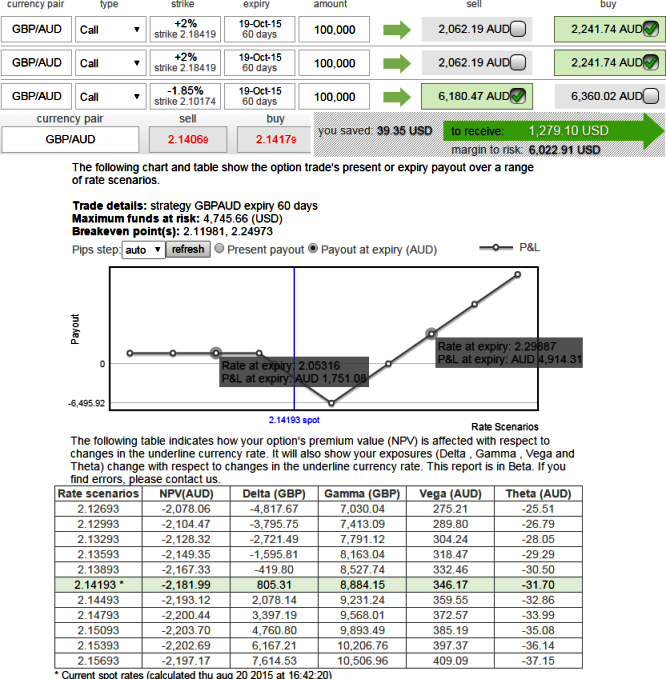

How can improve odds on GBPAUD call backspreads?

Delta & Gamma: As you can point out from diagrammatic representation of this bullish strategy, the spread is delta neutral through slightly positive (0.008) or close zero delta, while gamma is 0.08 which would imply that spread benefits if GBPAUD experiences upswings, if it drops down then there would be any harm to this portfolio but the profitability reduces.

Implied Volatility and Vega: The spread would gain from any increase in implied volatility as is evident from positive vega at 395.

When this position is executed, if within short term the underlying exchange rate progresses to OTM strikes (2.1841) where we added longs, this trade may actually be profitable if IV increases. But if it hangs around there too long, time decay will start to hurt the position. You generally need the stock to continue making a bullish move well past strike B prior to expiration in order for this trade to be profitable.

Threat for the position: Theta has been the real treat as the strategy contains more longs than shorts and theta has been negative here.

Hence, the maximum loss for the call back spread is limited and is taken when exchange rate of GBPUSD at expiration is at the strike price of the long calls purchased. At this price, both the long calls expire worthless while the short call expires in the money.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: Strategy optimizer through Black Scholes – a run through of GBP/AUD call backspread

Thursday, August 20, 2015 12:08 PM UTC

Editor's Picks

- Market Data

Most Popular