Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate

Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

EUR vol risk reversals remain low compared to the level of rates (refer above diagram). Also, in longer tails, the EUR volatility smile remains flat compared with the rates vs vol correlation seen since 2015 and over the past week (refer above diagram).

Despite the risk that the EURUSD correction goes further (it really hasn't gone very far yet), we're still very keen on EURJPY as a long-term long. As per the forecasts, a peak at 140 at the end of the year, and while that looks miles away it does remind that there is a lot to play for.

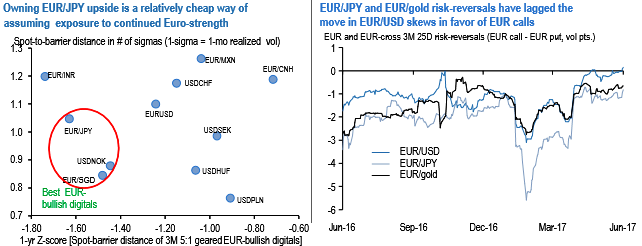

EURUSD risk-reversals flipped positive (bid for EUR calls) this week in sub-3M expiries in response to Euro strength, but there are still two laggards among Euro-crosses that are bid for EUR puts and have room to play catch-up if Euro strength continues: EURJPY (3M 25D r/r -0.8mid) and EUR/gold (3M 25D r/r -0.65 mid). Spot-vol correlation performed strongly positively this week and supports a narrowing of the EUR call discount: a 2.9% rally in EURJPY was accompanied by a 0.85 %pt. jump in 3M ATM, while a2.5% rally in EUR/gold led to a +0.4 vol uptick.

The obvious appeal of EUR-cross skews is that they earn smile decay while waiting for a re-pricing; they also avoid exposure to a Fed-driven bounce in the dollar, which isn’t looking much of a problem at the moment but has a low bar for resurfacing given the dollar’s substantial rates/FX disconnect and extended duration length in Treasuries.

According to JPM, the directional view of moderate gold weakness in H2 is more amenable to bullish Euro risk-reversal plays on crosses than the more constructive outlook on JPY, but even the latter may have room for near-term slippage amid widening Japan vs. rest of the world rate differentials and firmer equity market sentiment.

The steepness of the EURJPY risk-reversal curve renders back-end tenors better shorts, however, we prefer sticking to 2017 expiries (6M) since 2018 dates come with unpredictable Italian election risk. The EUR/gold risk-reversal curve is much flatter in comparison hence short tenors work fine. We enter short 6M 25D EURJPY risk-reversals (delta-hedged).