Morgan Stanley Downgrades Adobe, Workday as AI Transition Raises Growth Concerns

Morgan Stanley Downgrades Adobe, Workday as AI Transition Raises Growth Concerns  Bank of America Says These Overlooked AI Stocks Could Be the Next Winners

Bank of America Says These Overlooked AI Stocks Could Be the Next Winners  US Inflation Expected to Ease in June, but Fed Rate Hike Risks Persist Amid Middle East Tensions

US Inflation Expected to Ease in June, but Fed Rate Hike Risks Persist Amid Middle East Tensions  Morgan Stanley Says China’s Reusable Rocket Progress Poses Long-Term Challenge to SpaceX

Morgan Stanley Says China’s Reusable Rocket Progress Poses Long-Term Challenge to SpaceX  Gold Surges on Geopolitical Tensions: Buy Dips Toward $4205/$4300

Gold Surges on Geopolitical Tensions: Buy Dips Toward $4205/$4300

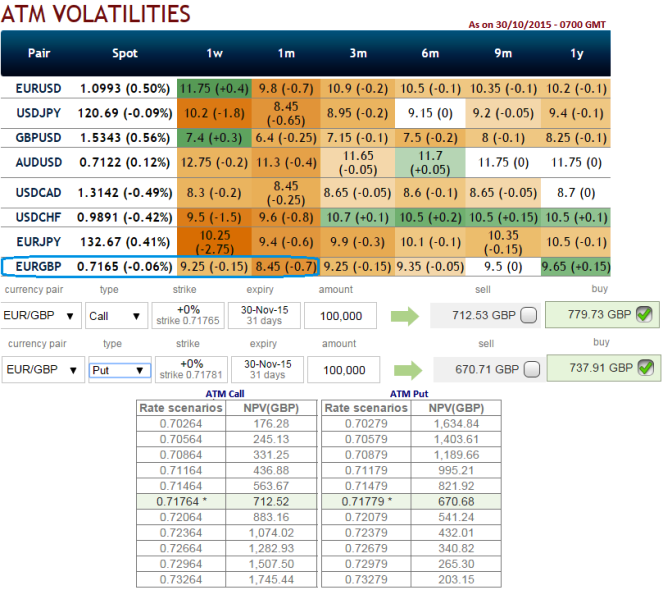

The implied volatility of ATM contracts is at 9.25% and it is expected to reduce at around 8.5% for near month expiries of this the pair.

NPV of 1m ATM call is at 712.52 while the Premiums trading above 9.40% at GBP 779.73 for lot size 100,000 units.

NPV of ATM put is at 670.68 while Premiums trading above 10.02% at GBP 737.91 for lot size 100,000 units.

Thereby, comparing this difference in options premiums and NPV with implied volatility in market sentiments we think the hedging cost would not be economical on downside deploying ATM put instruments.

But we cannot afford to get stuck in this riddle without hedging, so what's the alternative, in forwards markets at least..?

Subsequently, here comes the strategy arbitrage strategy in which options trading that can be performed for a riskless profit as EURGBP ATM call options are overpriced relative to the underlying exchange rate of EURGBP.

To perform this conversion, the hedger holds the underlying spot FX and offset it with an equivalent synthetic short spot FX (long put + short call) position.

Profit is locked in immediately when the conversion is done, the profit would be strike price of call/put - purchase price of underlying + call premium - put premium.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: EUR/GBP ATM puts seem costlier, option arbitration in lieu of shorts on reducing IV

Friday, October 30, 2015 1:30 PM UTC

Editor's Picks

- Market Data

Most Popular

7