Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data

The European recovery theme has become increasingly mainstream in recent weeks as continued Euro-area growth out-performance intersects with moderating political risks.

Last week, we opened an outright long EUR/USD position in covered call format to go with a suite of other bullish Europe expressions (long SEK, CHF).

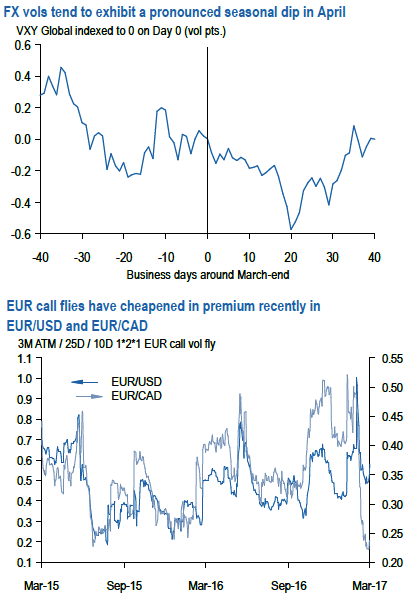

We list below a few other option-based expressions of Euro strength assuming that French elections deliver a market-friendly outcome: EUR call flies: Our spot targets for EURUSD if Le Pen loses are relatively benign – in the range of 2-3 cents from current levels since neither positioning metrics nor deviations from high-frequency fair value models suggest that there is much political risk premium in the currency that requires de-pricing.

In addition, EUR options still pack in a reasonable amount of election risk premium despite their recent softening, which will almost certainly disappear after the passage of the event – a key reason to recommend

As the VXY enters April near 2-yr lows having come off a full vol in March, it is hard to escape the sense that the timetable for the classic pump-in-April-dump-in-May pattern in risk markets is being pulled forward. Investors are well aware of the seasonal decline in FX vols in April (refer above chart) and the potential for pent-up demand for European and EM equities to fuel the next stage of the risk rally, yet are conflicted about value in short-selling options at current levels as the dollar’s cheapness vis-à-vis rates preserves the risk of a sharp snapback, trade/currency policy risks heat up next week onwards and ebbing momentum in commodities raises concerns that the reflation trade may be due a correction.

Our best guess is that risk markets will hold in and vols remain sideways to mildly lower into Easter, but remain wary of the possibility of a stray poll or TV debate to re-inject risk premium into Euro-pairs that has faded considerably in recent weeks.

The paucity of genuine value and lack of trends is not amenable to large risk allocations and leads us to trim a couple of soon-to-expire positions in our paper book (CADJPY – EURJPY gamma spread, EURCNH put spreads). This note remains deliberately focused on Europe which increasingly looks like the one durable macro theme worth allocating to. Sell CADJPY 1Y 25D RR via vanilla puts vs. sell EURJPY 1M ATM straddles, vega-neutral.