Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

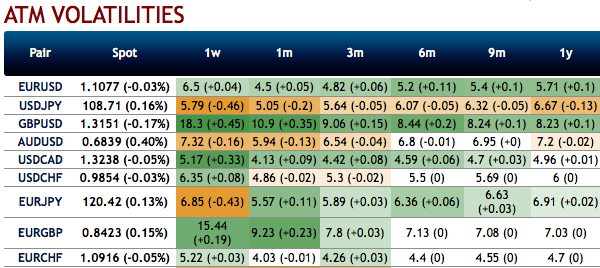

Amid low IV (implied volatility) environment, VXY Global heads into next year with the deepest cyclical undershoot on record, in excess of 3 % pts. The IVs of most of the FX pairs have been tepid, jerking in the range of 4-7% except cable and EURGBP.

The ultra-cheap vol valuations however need to be set in the context of less stressful global economic conditions next year. JPM baseline expectations of lukewarm moves from the big G3 FX, and the drip feed of USD strength in 2019 of the kind that erodes speculative interest in FX carry are other reasons to curb one's enthusiasm for a V-shaped vol rebound.

The path of least resistance to higher FX vol next year runs through politics (US/China, US elections), not economics.

Option themes for 2020:

1) The favoring EM vol over DM vol;

2) The betting on Euro strength through contained upside structures / RVs;

3) 2020 US elections: long USDCHF forward volatility over the Democratic primaries;

4) The systematic shorts in AUD and JPY risk- reversals as their risk-sensitivities have regime shifted lower;

5) Activate longs in GBPUSD 1Y1Y forward volatility for renewed back-ended Brexit disruption; and

6) The model-based mean-reversion pair selections (NOK vs. SEK, PLN vs. HUF). Courtesy: JPM & Saxobank