S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist

RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist  How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform

How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform  BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning

BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

The Federal Reserve last night maintained interest rates unchanged at 1-1.25%, as widely anticipated. The press statement was largely unchanged: it sounded a little more upbeat about recent economic developments, while still acknowledging some concerns about low inflation. A December rate rise is still likely, even though it was not explicitly signaled. Separately, President Trump is due to announce the next Fed Chair at 19:00GMT. His pick is expected to be Jerome Powell, who is a current Fed Governor, and would represent continuity in monetary policy. Powell is scheduled to speak at an event today.

BoE to pull the trigger: The BoE MPC is all set meet shortly and will probably raise rates by 25bps, marking the first rate hike in a decade. However, we question whether the MPC will have the opportunity to push through further rate hikes. A dovish hike (interpreted by markets as ‘one-and-done’) is likely to be neutral for Gilts and sterling.

We do not expect it to be a unanimous vote but the Bank of England MPC is expected to hike rates for the first time since 2007 at 12 PM (GMT) today. The rhetoric in the minutes has become more and more hawkish and the balance of other recent communications from members has reinforced the message that the committee is becoming increasingly uncomfortable with the current stance of monetary policy.

Firm growth, above target and still rising CPI (3% YoY in September) and a low unemployment rate makes the economic case for a hike. In addition, the market expects it, suggesting more disruption from a decision to hold than to hike.

As briefly alluded to earlier, the near complete pricing-in of next week’s BoE hike and the risk of dovish commentary in the wake of less-than-stellar cyclical dataflow leaves the pound vulnerable to an EUR-like drawdown.

Sterling isn’t a currency for high conviction capital commitment for most investors in light of the complicated twists and turns in monetary policy and politics, hence we suggest a low premium alternative of buying GBPJPY – USDJPY put switches to create synthetic short GBPUSD exposure.

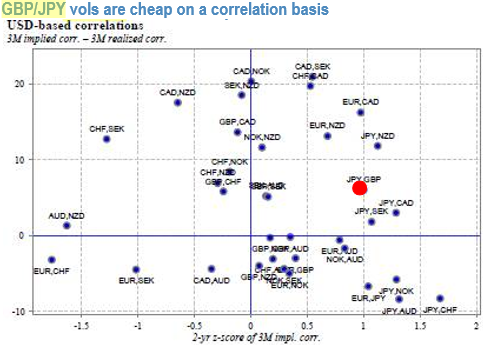

The RV rationale is that GBPJPY vols are cheap on a correlation basis (refer above diagram); the vol spread is a proxy for the selling the full USD-GBP-JPY correlation triangle.

Long GBP put/JPY call – USD put/JPY call 7-wk (15Dec17) 30D strike option spreads (strikes 146.50 and 112 off spot ref: 151.264 and 114.092) costs 12bp JPY in premium (equal JPY notionals/leg), much lower than the 115 bp GBP premium for an equivalent strike GBP put/USD call despite fairly conservative strike selection on the short USDJPY leg.

Currency Strength Index: Ahead of above stated BoE’s significant data event, FxWirePro's hourly GBP spot index is shy above positive -3 (which is neutral), while hourly JPY spot index was at -127 (extremely bearish), and USD at -7 (neutral) while articulating at 08:51 GMT. For more details on the index, please refer below weblink:

http://www.fxwirepro.com/currencyindex

FxWirePro launches Absolute Return Managed Program. For more details, visit: