Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields

Consumer prices (CPI inflation) in India came in softer than expected at 1.54 pct YoY, which was below market expectations of 1.7 pct and lower from 2.18 pct previously. The weakness was driven by food prices which fell 1.2% YoY. In the CPI basket, food and beverages account for 54% of the basket.

The fact that inflation dipped below RBI’s 2-6% medium-term target reinforces expectations of RBI resuming rate cuts as early as the next meeting on 2-August. The market is pricing in around 60% chance of a 25bp rate cut to 6%.

At this stage, RBI may take a cautious stance and not signal the start of aggressive rate cuts ahead. This is because of the push for banks to clean up the balance sheet and deal with bad debts rather than to make it easier for unviable companies to stay afloat with lower rates.

Nevertheless, the risks will be for more rather than less cuts if inflation continues to undershoot RBI’s forecast of 3.7% for the current fiscal year. For USDINR, it held steady yesterday around the 64.54 level and still within the 64-65 consolidation range.

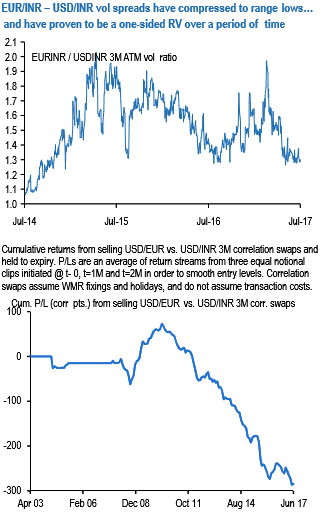

EURINR – USDINR vol spreads have compressed to levels that strike us as decent buys (refer above chart). This runs counter to our overall bias to own USD-correlations by buying USD-vols and selling cross-vols as outlined in recent weeks, as per the JPM.

Reasons notwithstanding, long EURINR vs Short USDINR fits the profile of a systematically profitable vol RV, with a lop-sided implied vs. realized vol set-up and a track record of successful one-way P/Ls over the past decade (refer above chart).

Risk reversals are even better placed than ATMs to play the RV since EURINR skews are marked 0.4-0.5 vols under USDINR skews across the curve even after the recent uptick in EUR-cross riskies; we advocate a reduced form expression of the skew RV via EUR call/INR put –USD call/INR put switches that are 0.3-0.4 vol discounted vis-à-vis ATM strikes.

We favor a 10-wk option tenor that that increases odds of leveraging any ECB-led gamma spikes by spanning the crucial September meeting where QE tapering is expected to be announced, but expires before the FOMC meeting later in the month and sidesteps balance sheet normalization-related noise on the USD-leg.