The government is ‘doubling down’ on its social media ban. But bigger penalties for platforms aren’t enough

The government is ‘doubling down’ on its social media ban. But bigger penalties for platforms aren’t enough  A Korean Family Spent 34 Years Hoarding Chinese Tea. Now They're Putting It on the Blockchain.

A Korean Family Spent 34 Years Hoarding Chinese Tea. Now They're Putting It on the Blockchain.  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  Should I take zinc or eat oysters to ward off colds, boost my immune system or improve fertility?

Should I take zinc or eat oysters to ward off colds, boost my immune system or improve fertility?  Buy the Dip: Gold Holds Strong at $3980, Targets $4150

Buy the Dip: Gold Holds Strong at $3980, Targets $4150  Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns

Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns  Morgan Stanley Names BAE Systems Top European Defence Stock Despite Lower Price Target

Morgan Stanley Names BAE Systems Top European Defence Stock Despite Lower Price Target  Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand

Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand  Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum

Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum

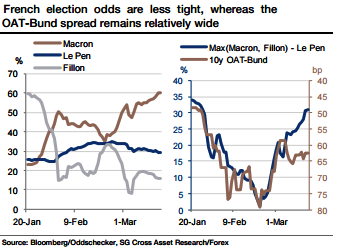

The political risk is tracked by the bookmakers odds, where the probability of a Le Pen win is stable around 30% (please refer above graph).

The medium/long-term impact on euro crosses highly depends on the materialization of a Frexit scenario. The impact of the French election is going to be extremely asymmetric on euro crosses, depending on the pro- or anti-Frexit outcome.

On the back these expectations, and in the aftermath of the Brexit vote and the Trump election, such a scenario cannot be qualified as a tail risk (unlike an actual Frexit). The OAT-Bund 10y spread has been closely following the spread between the winner’s odds and Le Pen’s odds (please refer above graph).

But there is now some risk premium in the bond market since Macron’s odds rose while the OAT-Bund spread did not materially tighten.

Indeed, there is much more volatility in Fillon and Macron voting intentions compared to Le Pen, keeping the market on guard.

All in all, the OAT-Bund spread should remain the best gauge for political risk and can be used to find the best FX hedge.