3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online  Gold Loses Momentum as Yields Rise and Safe-Haven Demand Fades

Gold Loses Momentum as Yields Rise and Safe-Haven Demand Fades  Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be  Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Last week EIA reported crude oil inventory at 8.0M which was a rise from previous 7.6M, as a result crude prices began dropping which in turn led to NOK's losses. This depreciation in NOK in H2 2014 has underpinned inflation, but slower growth and lower domestic demand will drag prices lower once the FX effect starts to wane.

While oil prices will dictate the short term moves in NOK, the longer term NOK outlook will depend on the lasting effects of lower oil prices to domestic drivers.

Providing support to domestic growth though is Norway's fiscal rule and the translational effect of a weaker NOK on Norway's sovereign oil fund, GPFG, that act as an automatic stabilizer.

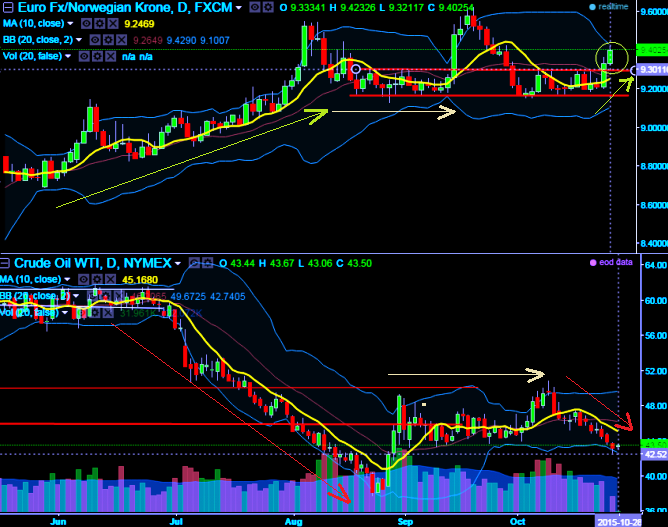

We can observe from the diagram how this currency cross is directly proportional to the oil prices.

NOK weakened sharply as crude oil benchmarks pushed to significant new lows today, while EURNOK managed to clear the 9.30 resistance, shifting the focus back higher.

NOK hit by renewed crude oil selloff, EURNOK clears 9.30 resistances.

This FX translational effect would have increased the government's fiscal scope by NOK 30bn in 2014, i.e., about 1% of mainland GDP-sums which the government can use to prop up the economy.

As such, we are cautiously constructive on NOK and believe EUR/NOK can drift lower once oil prices are able to find a stable floor.

Hence, only a material recovery in oil prices is likely to stop those cutting rates to new historic lows.

While this risk overhangs, we maintain a negative stance on the currency, with EUR/NOK expected to retest the recent highs around 9.60.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: NOK likely to extend losses on the back crude supply glut – EUR/NOK heading towards H2 targets at 9.60

Wednesday, October 28, 2015 11:33 AM UTC

Editor's Picks

- Market Data

Most Popular

1