Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning

BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning  Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940  Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations  BOJ Rate Hike Expectations Rise Ahead of September Meeting

BOJ Rate Hike Expectations Rise Ahead of September Meeting  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure  Same sparkle, different story: how lab-grown diamonds are transforming the market

Same sparkle, different story: how lab-grown diamonds are transforming the market  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

The Polish zloty has staged an impressive recovery over the past fortnight, strengthening from a low of 4.40 against the euro in early July to near 4.2870 at present (while articulating). Polish policymakers have commented that they expect around 5% GDP growth for Q2 (the same as in Q1). The confidence in a solid growth outlook has been a notable feature of the Polish business landscape over the past year, and this has been a supportive factor for the zloty.

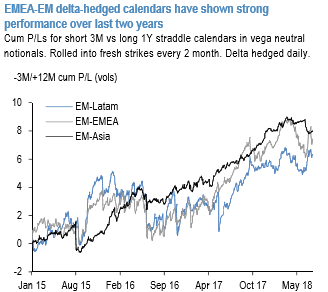

Historically, short gamma, vega neutral structures of the type short front / long back vol have performed well within EM where spot tends to be under the watchful eye of central bankers while most of the market pricing gets filtered into back tenors. Within EM, EM Asia has been the most consistent outperformer but EM-EMEA also have shown strong average with an overall Sharpe ratio of 0.7 for short 3M/long 12M delta hedged straddles over the last 3-years.

Despite the adverse trade tariffs developments, cross-asset vols dropped since early July, characterizing risk supportive market sentiment. That could also be a relevant factor for containing the marked drop of EM currencies that started in early April and for suppressing realized vols/front-end of the curve.

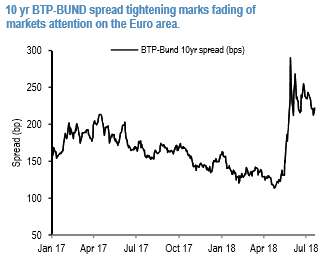

Further support for EURPLN vol selling should come from traditionally lighter summer calendar over next 2 months and as markets attention on the Euro area is fading at the moment (see 10 yr BTP-BUND spread tightening in refer below chart), and EURPLN is less correlated with global risk factors than eg. USDPLN.

Even at the currently elevated levels realized vol is trailing implied vol by 0.5vols and high frequency (hourly) realized vol is indicating softer realized vol going forward.

The forecasts presume that this pace of growth would not last during the coming quarters – latest data strengthen this view, and although growth may not be the primary driver of the exchange rate, the data support our story of a weaker zloty over the coming year.

Zloty should be relatively less impacted to increased trade tensions in the auto sector (with about four times less export/GDP exposure than Hungary or the Czech Rep) and list PLN as they favoured OW within CEE. Positive macro and fundamentals should be supportive of short front vol.

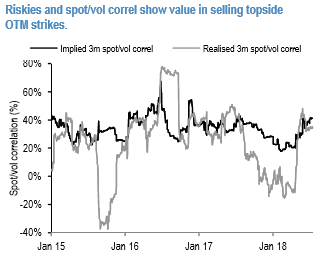

With respect to strike selection, 3M EURPLN risk reversals seem elevated by historical standards and the implied spot/vol correl is now modestly rich to realized spot/vol correl following the recent consolidation of the realized spot/vol April jump, making selling OTM strikes a viable option (refer below chart).

The curve inversion (refer below chart) is supportive of long vega, overall making short 2M 25D calls vs. long 6M straddles in vega notionals our favorable EURPLN vol calendar expression. Sell 2M 25 delta EURPLN calls @6.8/7.225indic vs buy 6M EURPLN straddles @5.975choice, both legs delta-hedged, in vega notionals.

Currency Strength Index: FxWirePro's hourly EUR spot index is inching towards -37 levels (which is bearish), while USD is flashing at -82 (which is bearish), while articulating at (11:02 GMT). For more details on the index, please refer below weblink: