Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  ‘Vibe coding’ is fun and easy, but there’s a major catch

‘Vibe coding’ is fun and easy, but there’s a major catch  3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data

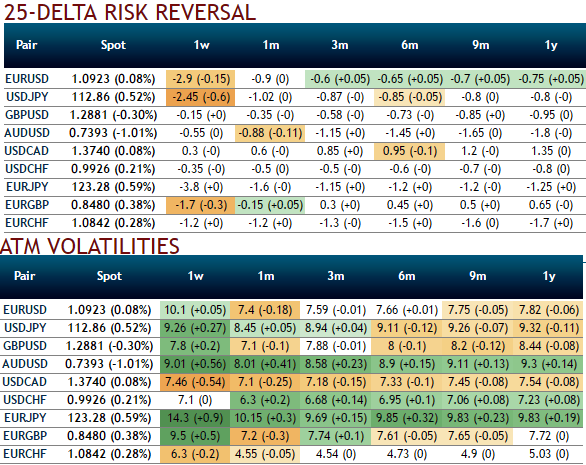

Please be advised that the 25-delta risk of reversal of GBPUSD has not been indicating any dramatic shoot up nor any slumps but bearish-neutral (no fresh change in risk reversals has been observed), but seems to be one of the pairs to be hedged for downside risks as it indicates puts have been relatively costlier.

The risk reversal curve has been traveling in a linear direction, while spot curve is slumping downwards back to converge with the RR curve. While implied volatilities across all tenors have been shrunk massively.

Sterling fell pretty much with interest rate expectations after the vote to leave the EU in June. If we look at 3m futures contracts, there’s been a 60bp shift in relative pricing of where rates will be in a year’s time that reflects consensus now that fed funds will be at 1-1.25% in December 2017, while UK rates will be unchanged at 0.25%. This is in line with our forecasts and points to a period of relative calm for the pound (which is currently seeing some much-needed short-covering) before the economic implications of leaving the EU to become clearer.

We will fade the short covering: A period of calm, however, can turn into renewed weakness if the squeeze on real incomes undermines the recovery in economic confidence and upward revisions to growth forecasts. So while we expect GBPUSD to trade in between 1.3473 on northwards and 1.25 on southwards for next 6m or so, we are wary of spikes above 1.3473 in medium term perspective and expect to see a temporary return to 1.2650 at some point.

Brexit has hurt eventually no matter if it is going to be soft or hard exit: If we do see resilience for sterling through 2Q, as UK data hold up, and if we also see the euro trade down to parity with the dollar over that timescale, we would look to buy EURGBP for a sharp rebound in 2Q-3Q as UK growth suffers from higher inflation, and the political tailwinds facing the euro fade. A return to levels above EURGBP 0.88-89 seems to be pretty much possible in 2017.

Scandinavian currencies to fare better: GBP bears may also find that shorts in GBPSEK and GBPNOK bear fruit in rest of 2017 despite momentary spikes, as higher inflation globally would trigger a shift in the stance of monetary policy in Scandinavia.

While the cable volatility surface has returned to levels seen at the start of the year overall, but risk reversals and butterflies are now excessively cheap: - The sell-off in the cable skew is exaggerated compared to ATM volatility, since the risk remains asymmetric on the downside; - The tail risk is mispriced, as the GBPUSD butterfly is now less expensive than the EURUSD butterfly, which is unsustainable given the GBP extra tail risk.