Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022

Natural gas is currently trading at $3.17 per MMBtu.

Key factors at play in the natural gas market –

- After a sharp rise the price of natural gas in the United States is moving lower again, however, the price could spike higher with the approaching winter and lower level of inventories providing bullish support, along with higher price outside the U.S.

- The United States and the European Union have agreed in principle in bringing U.S. LNG to Europe.

- China surpassed Japan as the biggest natural gas importer.

- Russia says that the biggest pipeline project reaching China is almost over.

- Japan’s nuclear power generation is reviving again, which would curtail the LNG demand.

- Gas price remains high, globally, especially in Japan and in Europe. However, in the United States, we expect the natural gas price to decline further towards $2.55 area, largely due to the existing bottlenecks in global trade.

- Price in Europe is breaking into record highs but currently declined to 67 pence a therm. Russia and the United States are set to fight for market share in Asia and in Europe. US preparing to become major natural gas exporter to the EU and Asia.

- Large Natural gas producers in the United States continue to expand production per rig. US exports are increasing significantly. The United States remains the largest petroleum and natural gas producers in the world.

- U.S. production is rising fast. Currently, U.S. is the third biggest exporter of natural gas.

- U.S. exit from Iran nuclear agreement complicates the future of vast natural gas reserves in Iran. Recently, French energy giant ‘Total’ exit lucrative Iran gas project amid sanctions.

- NATO sanctions on Russia might disrupt its gas supplies to Europe.

- Russia is likely to dominate the Chinese gas market, fastest growing in the world.

- With natural gas turning into a buyers’ market, big importers like Japan are renegotiating long-term contracts with a resale clause attached.

Now, for the inventory,

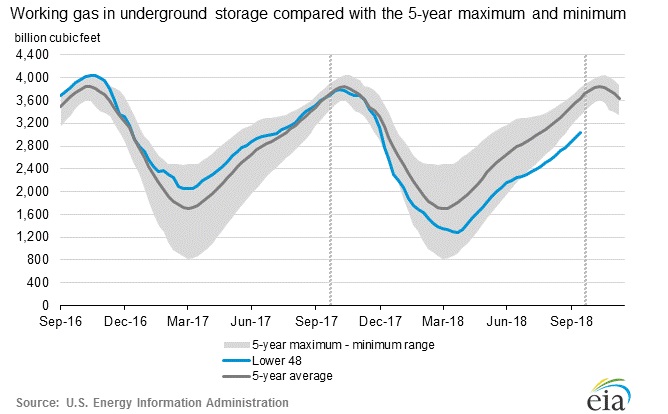

According to the latest numbers, working gas in underground storage remains at 3.037 trillion cubic feet (Tcf). Stocks are 601 Bcf less than last year at this time and 605 Bcf below the five-year average. The chart from EIA shows the level of inventory. The second chart from investing.com shows weekly changes in inventory.

- Last week, the inventory rose by 81 billion cubic feet against an expectation of 87 billion cubic feet increase. Today 81 billion cubic feet build expected.

- EIA will release the inventory report at 14:30 GMT.