EUR/JPY Bulls Charge: Eyeing 186.00 as Euro Strength Intensifies

EUR/JPY Bulls Charge: Eyeing 186.00 as Euro Strength Intensifies  FxWirePro: EUR/AUD gaining momentum for a move towards 1.6800 level

FxWirePro: EUR/AUD gaining momentum for a move towards 1.6800 level  Aussie Retreats Against the Yen: AUDJPY Bears Target 108 as 110 Resistance Holds Firm

Aussie Retreats Against the Yen: AUDJPY Bears Target 108 as 110 Resistance Holds Firm  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  FxWirePro- Major European Indices

FxWirePro- Major European Indices  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  FxWirePro: USD/CAD runs out of steam but maintains bullish outlook

FxWirePro: USD/CAD runs out of steam but maintains bullish outlook  FxWirePro: GBP/USD recovers but bears are not done yet again

FxWirePro: GBP/USD recovers but bears are not done yet again  Bitcoin Battles Volatility: Institutional Support Eyes USD 64,000 Floor Amid Geopolitical Tensions

Bitcoin Battles Volatility: Institutional Support Eyes USD 64,000 Floor Amid Geopolitical Tensions  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  FxWirePro: GBP/NZD range to extend until there is game changing news

FxWirePro: GBP/NZD range to extend until there is game changing news  FxWirePro: USD/JPY firms as Trump's address on Gulf war spark fresh concerns

FxWirePro: USD/JPY firms as Trump's address on Gulf war spark fresh concerns  FxWirePro: AUD/USD downside pressure builds, key support level in focus

FxWirePro: AUD/USD downside pressure builds, key support level in focus  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  NZDJPY Bears Take Control: New Zealand Dollar Retreats as 92 Resistance Holds Firm

NZDJPY Bears Take Control: New Zealand Dollar Retreats as 92 Resistance Holds Firm

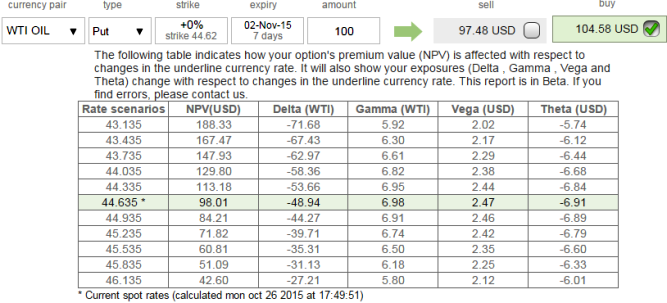

Let's suppose, as shown in the diagram, we have vega of at the money WTI put option at 2.47 with implied volatility at 20% which is now trading at US$104.38.

This would mean that the chances of upside risks of option prices to reduce by US$49.4 if the underlying commodity price rallies and the other way round.

Option premiums behave with this reasoning, vertical bear put spread strategy is employed when the options trader thinks that the price of the underlying WTI crude will fall reasonably in the near term but within a bracket of 3% downward range.

Rationale: Always remember the option's delta and vega would have the huge impact on a long put position should the market bounce.

So the recommendation would be "long vertical put spread" that will cuts down the exposure you have against dubious rallies in anyone's mind, but more significantly it will also reduce the exposure you have to Vega, the relative effects of volatility on the option prices.

One way of minimizing the avid appetite with a naked long put has for your precious capital is to spread much of the risk by using vertical spreads.

Hence, we constructed the above strategy by shorting (-3%) deep Out-Of-The-Money put with the same maturity so as to turn vega into correspondingly positive.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: Vertical spread to reduce WTI vega risks

Monday, October 26, 2015 12:39 PM UTC

Editor's Picks

- Market Data

Most Popular

6