China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow

BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025

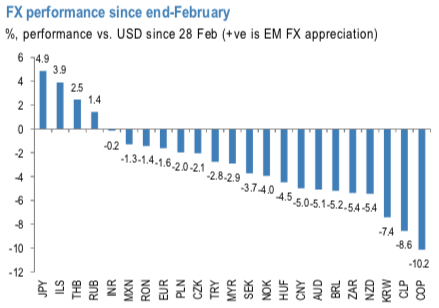

The underperformance of South African local markets the past several months has been remarkable. Despite the dovish shift of the Fed and the SARB interest rate cut, since the start of March (prior to the beginning of the current phase of the global bond rally), the currency has lagged the performance of high yielding peers including Brazil, Mexico, Russia, and India (refer 1st chart).

A narrative shift is underway and mixes uncomfortably with stretched SAGB positions. It is not difficult to explain the recent poor performance of South African local markets given the market’s focus on fiscal woes. The fact remains, however, that South Africa is not the only emerging market with difficulties; one could argue that the rand’s role as a liquid “EM proxy” could have resulted in greater outperformance in the period of positive EM local market returns prior to the re-escalation of the US-China trade war this week. What gives? We suspect that a broader ‘narrative shift’ is underway; one which alters the risk characteristics of local assets and the lens through which investors view South Africa in a profound way.

The risk-reward of ZAR has already changed. One way to illustrate our argument that the shift of investment narrative is altering the risk-reward characteristics of the rand is to compare the currency’s performance in periods of EMFX strength and weakness (refer 2nd chart). While ZAR's 'high beta' nature has been symmetric over the long-run (1.44 beta whether the market is up or down), more recently, ZAR has tended to sell-off almost twice as much on days of broad EMFX weakness as compared to days of EMFX strength.

In other words, ZAR returns about as much as the broad EMFX index on days of EMFX appreciation (beta of 1.09 YTD), but loses twice as much as the index on days of EMFX depreciation (beta of 1.90 YTD).

Against this backdrop, we hold on to our structural bearish positions. We also recommended a 3m 14.75 USDZAR call at the end of July 23rd. The sell-off has been fast, with ZAR around 8% weaker vs. the USD since JP Morgan’s options trade monitor.

Normally, we would expect the momentum of the sell-off to abate after such a move and we will watch the market closely for signs of positioning becoming stretched. However, the starting point appears to have been a long ZAR speculative position, in our assessment. Courtesy: JPM