FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022

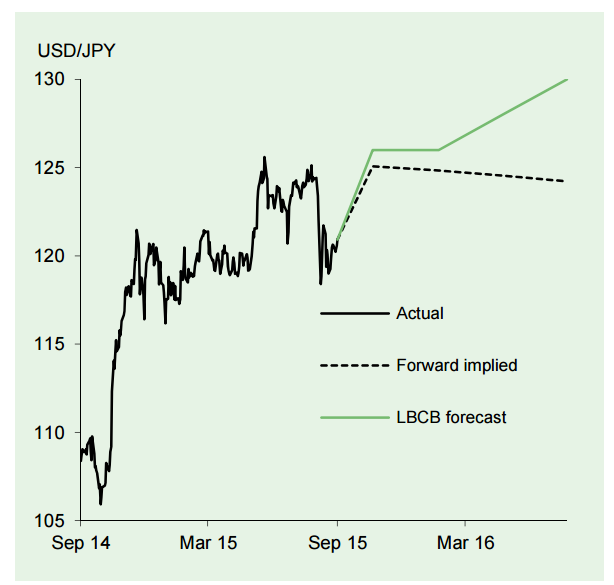

As witnessed on many occasions previously, a sharp sell-off in global equity markets helped to bolster the Japanese yen, with USD/JPY briefly spiralling below 116.10 on 24 August, from above 124 only the week before. An improvement in risk sentiment since, largely owing to signs of financial market stabilisation in China, saw USD/JPY climb back 120.

External developments and market volatility represent the key drivers for the yen in the near term, with China and the timing of the first rate hike in the US considered the two main influences. Meanwhile, the domestic economic situation remains disappointing, supporting the case for continuing massive monetary stimulus to combat entrenched deflationary pressures.

The economy contracted by 0.3% in the second quarter, leaving open the prospect of the BoJ adding to its easing measures, possibly as soon as next month. This will keep fundamental downward pressure on the yen, particularly against currencies where monetary tightening is soon expected.

"We forecast USD/JPY at 126 at end year and 130 at end 2016", says Lloyds Bank.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

USD/JPY Outlook

Wednesday, September 23, 2015 10:36 PM UTC

Editor's Picks

- Market Data

Most Popular