Oil Prices Ease as Markets Weigh U.S.-Iran Peace Deal and Strait of Hormuz Reopening

Oil Prices Ease as Markets Weigh U.S.-Iran Peace Deal and Strait of Hormuz Reopening  Yen Near 40-Year Lows Despite BOJ Rate Hike, Markets Brace for Possible Intervention

Yen Near 40-Year Lows Despite BOJ Rate Hike, Markets Brace for Possible Intervention  Gold Prices Rebound on U.S.-Iran Peace Deal Optimism Despite Fed Rate Hike Signals

Gold Prices Rebound on U.S.-Iran Peace Deal Optimism Despite Fed Rate Hike Signals  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Europe EV Demand Surges as Fuel Prices Rise Amid Iran Conflict

Europe EV Demand Surges as Fuel Prices Rise Amid Iran Conflict  ASX Proposes New Share Dilution Limits for Public Takeovers

ASX Proposes New Share Dilution Limits for Public Takeovers  Asian Stocks Advance as Nikkei Nears Record High Ahead of Fed Decision

Asian Stocks Advance as Nikkei Nears Record High Ahead of Fed Decision  Japan Signals Readiness to Intervene as USD/JPY Nears 161 Amid Yen Weakness

Japan Signals Readiness to Intervene as USD/JPY Nears 161 Amid Yen Weakness  Asian Stocks Surge as Oil Prices Fall and Strong US Dollar Weighs on Markets

Asian Stocks Surge as Oil Prices Fall and Strong US Dollar Weighs on Markets  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX  German Industry Employment Falls to Lowest Level in a Decade

German Industry Employment Falls to Lowest Level in a Decade

The tepid expansion among EMs is unlikely to stymie growth within advanced nations, where domestic spending has accelerated noticeably. U.S. domestic demand growth has been hovering at 3% for more than a year, reinforcing the notion that the economic drivers are mainly focused inward for America at this point in the cycle. The sizeable appreciation in the greenback is expected to continue to dampen exports, but the broader economic foundation is strong enough to support a modest degree of rate hikes.

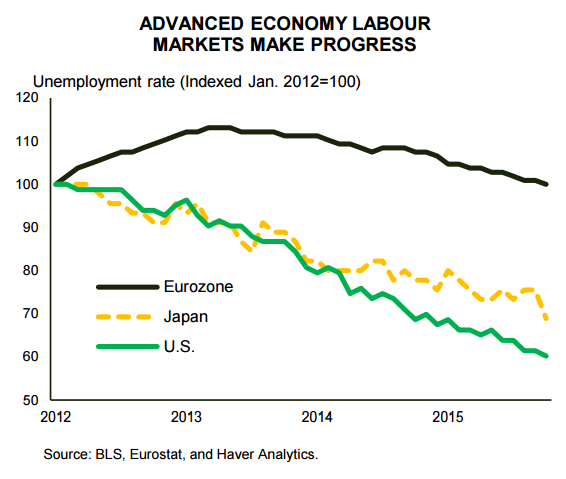

The beleaguered euro zone did manage to outperform the growth expectations. Surprisingly perhaps, in a year that featured fears of a "Grexit." However, unlike the U.S., the European Central Bank (ECB) is still stepping on the stimulus-accelerator to lift domestic demand through a combination of quantitative easing and negative interest rates. Private sector lending has been responding and unemployment rates are falling through most of Europe. Both of these positive trends should help to underpin continued gains in domestic demand going forward. The euro area should benefit from a slight tick-up in growth to 1.7% in 2016, a testament that the region has come a long way from the dismal 2014 performance that was roughly half this pace. However, the outlook remains heavily dependent on a central bank that is unlikely to lift its foot off the monetary accelerator.

Past stimulus initiatives in Japan are also starting to bear fruit. After a 0.7% increase this year, Japan is forecast to grow at a faster 1.2% pace in 2016. That may sound slow, but it is fairly good for an economy whose working age population is falling by 1.5% each year. That reality makes Japan's recent solid employment growth more impressive, as it comes from rising labor force participation.

As a large energy importer, Japan has also enjoyed a big boost to its purchasing power due to lower oil prices. All of these forces should help sustain the domestic economy in the face of softer EM demand, although a planned sales tax hike in 2017 is expected to crimp overall GDP growth in that year.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Advanced economies continue to make progress

Thursday, December 17, 2015 11:50 PM UTC

Editor's Picks

- Market Data

Most Popular