Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

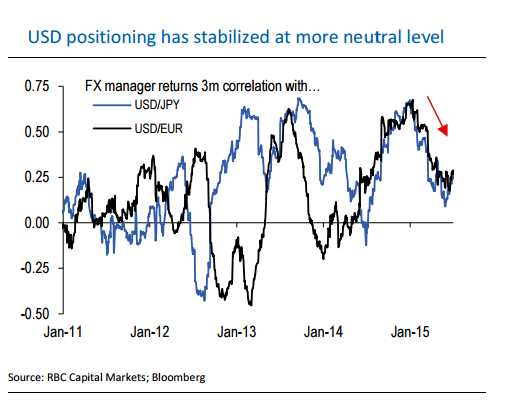

RBC Capital Markets notes:

1-3 Month Outlook

For the last 2-3 months, USD has been going sideways. It peaked in March, when markets were pricing in the first rate hike by September, but USD has retraced since then, in line with rate expectations that have also been pushed back . For the last few months, there has been a steady drift in the US forward curve - as we roll forward a month, the market consensus for the first Fed hike does the same. Meanwhile positioning has stopped falling but has stabilised at relatively low levels compared to the extreme USD longs seen at the start of the year.

But US data continue to improve. Our US ESI has been in positive territory for the past month (more upside than downside data surprises), having been in negative territory from mid-February until early June. And even FOMC members themselves are tilted towards a September hike - based on the dot plot, 60% of Fed members are pencilling in at least two hikes this year (Sept and Dec) and 90% are looking for at least one hike. If the Fed skips September, our economists' base case for Fed lift-off will shift all the way out to 2016 as they argue year-end liquidity concerns will make the odds of a December start to tightening very low.

Along these lines, we think the odds of a scenario where the Fed starts in September and pauses are higher than starting in December. As long as we are on track for a September hike , we see potential for USD to make further gains into the end of this quarter. Technically, DXY has already broken above key resistance (100dma, prior highs, and trendline) indicating a re-invigorated upswing toward 97.775 (May highs). Above there, stronger resistance is found near the 2015 highs between 99.99 and 100.39. Initial support is at the 50dma at 95.29. The larger bull trend is still defined by the 200dMA at 92.85.

6-12 Month Outlook

Longer-term, we remain USD positive, though the pace of gains should moderate. There is some risk that if the Fed does not hike in September, it pushes that back into 2016, which would also delay further USD gains. But we are still comfortable in calling for further USD gains, particularly against JPY. While we have heard more Fed officials complain about USD strength, we think the US is well-placed to shoulder modest currency appreciation. Our forecasts are unchanged.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Currency Outlook: US Dollar

Monday, July 6, 2015 11:19 PM UTC

Editor's Picks

- Market Data

Most Popular