FxWirePro: USD/ CNY hits one-month low,scope for futher downside

FxWirePro: USD/ CNY hits one-month low,scope for futher downside  FxWirePro: USD/JPY edges higher as focus shifts to BOJ decision

FxWirePro: USD/JPY edges higher as focus shifts to BOJ decision  NZD/JPY Flatlines Near 94.60: Will Key Support Reignite the Uptrend?

NZD/JPY Flatlines Near 94.60: Will Key Support Reignite the Uptrend?  AUD/JPY Slips Below 112 as BOJ Intervention Sparks Bearish Momentum: Sell the Rallies

AUD/JPY Slips Below 112 as BOJ Intervention Sparks Bearish Momentum: Sell the Rallies  JPY Action Bias: EURJPY and CADJPY Emerge as Extremely Bullish Pairs to Watch

JPY Action Bias: EURJPY and CADJPY Emerge as Extremely Bullish Pairs to Watch  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  FxWirePro: GBP/AUD drifts lower after BOE rate decision

FxWirePro: GBP/AUD drifts lower after BOE rate decision  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  FxWirePro: USD/CAD slips after Fed holds rates steady

FxWirePro: USD/CAD slips after Fed holds rates steady  Major Forex Pairs Action Bias: GBPUSD and AUDUSD Turn Extremely Bearish

Major Forex Pairs Action Bias: GBPUSD and AUDUSD Turn Extremely Bearish  EURUSD Spikes to 1.14306 on Fed Pause as Traders Eye Sell-the-Rally Setup

EURUSD Spikes to 1.14306 on Fed Pause as Traders Eye Sell-the-Rally Setup  FxWirePro: GBP/AUD gains above 1.9200 level , upside pressure builds

FxWirePro: GBP/AUD gains above 1.9200 level , upside pressure builds  FxWirePro: EUR/AUD regains upwards momentum but unable to hold above 50%fib level

FxWirePro: EUR/AUD regains upwards momentum but unable to hold above 50%fib level  Buy the Dips on EUR/JPY: Bullish Structure Points to 188 Target Ahead of Fed

Buy the Dips on EUR/JPY: Bullish Structure Points to 188 Target Ahead of Fed  FxWirePro : GBP/NZD strongly bearish despite upside attempts

FxWirePro : GBP/NZD strongly bearish despite upside attempts  FxWirePro: AUD/USD dips below lower range, bearish bias increases

FxWirePro: AUD/USD dips below lower range, bearish bias increases

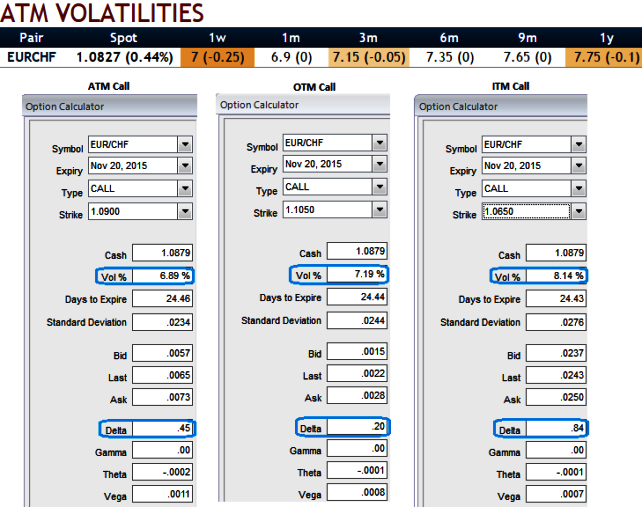

In a true smile, options with an at-the-money strike are priced with a lower volatility than out-of-the-money and in-the-money volatility strikes. Such market occurrences are observable in the EURCHF FX OTC market.

For instance, suppose we've constructed an at the money call option of EURCHF with this month expiry and with this given maturity has an implied volatility of 7% (6.89% to be precise, and that its delta amounts close to 50%.

We ponder now with an another call option with the same maturity on the same pair is priced with an implied volatility of 7.15% but its strike is 2% out of the money (strike at 1.1050) and while its delta is just shy of 20%.

Furthermore, let's contemplate a 3rd option with a strike in the money strike and a delta of 80% is also priced with a volatility of 8%.

On a 1-3m horizon, our target for this pair is still higher though we have adjusted our Q4 forecast (at 1.10) but certainly not with steep moves. Fundamentally, the latest quarterly SNB meeting also did nothing to change the currency outlook.

The inflation forecast was revised lower again in the near-term (on lower energy prices) though the long-term forecast was little changed.

Although EUR/CHF reached a new post-floor high in the beginning September (at 1.1049), the pace of appreciation is painfully slow, Infact the fluctuation has been softened.

We have positioned for higher EUR/CHF in options with a risk reversal but the long tenor (1y at entry, expiring July 2016) shows how long we expect this process to take.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

EUR/CHF creeps up with snail’s pace - volatility smiles suggest ATM instruments

Tuesday, October 27, 2015 1:57 PM UTC

Editor's Picks

- Market Data

Most Popular

1